#16: Portfolio Update 2Q21 Earnings

More adtech players enter public market arena; Chum bait is still chum bait; Next Fifteen Communications added to our agency portfolio.

Welcome to Quo Vadis, your periodic source for fresh programmatic news and off-the-beaten-path perspective. Click here to join the conversation.

We took a little summer break to charge our batteries but kept our eye on the programmatic scene from afar. And what an eventful few months it’s been! As Q2 earnings have now come and gone, several adtech newbies have entered the public arena making IPO’s look easier than ever.

We recommend turning up your volume on Electric Light Orchestra’s “Easy Money” to get the most out of this issue.

“Wake” of New Adtech Players Enter Public Market Arena

Term of the Day [wake] — A “wake” is a group of perched turkey vultures. Imagine them mourning over something with their heads hung down. Read more at Audobon.org. Just like programmatic companies, they are super interesting creatures!

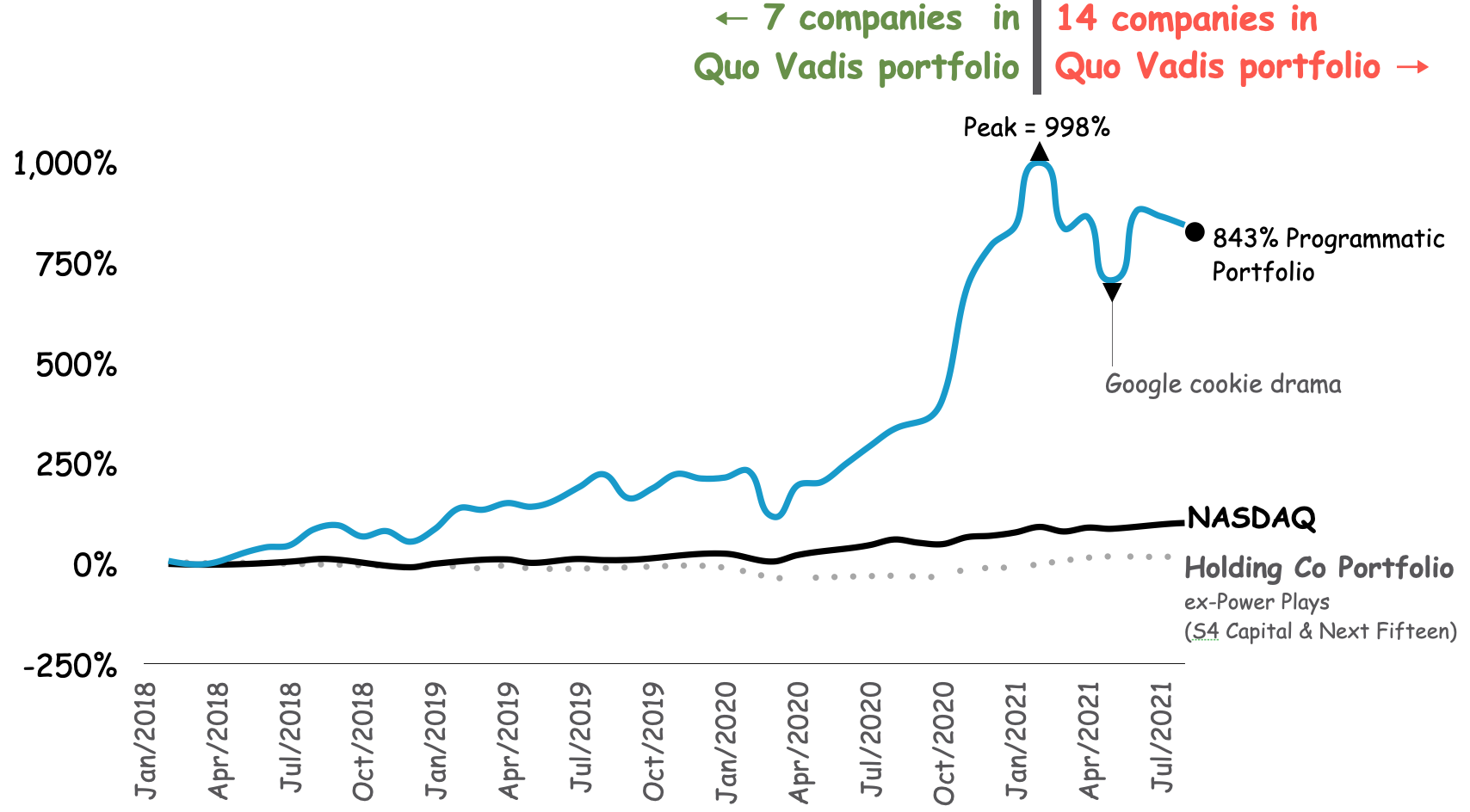

We started our equal-dollar programmatic portfolio in March 2021 with just 6 companies — TradeDesk, Criteo, Liveramp, Magnite, Roku, and S4 Capital.

My (oh my), how time flies… just 2 quarters later and we now have 14 programmatic-reliant companies in play. No doubt, they’re all jockeying to attract as much ad budget as possible from marketers. They’re also racing to source whatever inventory they can find (cough...Taboola and Outbrain).

We also added Next Fifteen Communications (NFC) to our agency holding company portfolio. NFC is a new-age holding co similar to S4 Capital and You & Mr. Jones (which is still private, but for how long?)

Portfolio Rundown

Overall, our programmatic portfolio is up 843% since January 2018. In other words, had you bet $100 on the basket of 5 original stocks in January 2018 — adding S4 Capital in September 2018 as we did — and then added 8 adtech newcomers, you’d have $743 of extra cash in your pocket today (don’t forget to subtract your original $100 investment).

Mind you, had you sold the entire portfolio in February 2021 before Google threw monkey wrenches in programmatic’s cookie machine (and at Pubmatic’s post-IPO bump price), you’d have an extra $155 in your pocket.

Portfolio Newbies: Investors Mind the Gap

If one thing is becoming more clear in the data, it’s this: the older the company in our portfolio, the more confidence investors seem to have in management’s ability to roll with the punches and keep pace with the earnings treadmill. Everyone else is going to need to fight like a wake of scavengers just to pick up programmatic scraps.

And if the risk-free interest rate ticks up along with equity risk premium (ERP), many of these companies will not be able to deliver sufficient returns on capital, let alone top-line growth.

Portfolio Timeline

Our Quo Vadis programmatic portfolio has four categories of companies:

Demand-side Platforms (DSP) — buyers work with these players

Supply-side Platforms (SSP) — sellers (and increasingly more buyers) work with these players

Data / Verification Vendors — Data Providers and Data Sellers are the nuclei of programmatic audience targeting. Verification Vendors monitor the resulting ad quality reporting on factors such as human/not human, viewability, and brand safety. Think of these players like Moody’s or S&P rating mortgage-backed securities, but they rate ad quality instead. Marketers certainly hope these independent homework graders give A-ratings to A-class ad quality more than they give A-ratings to D-class quality.

Agencies — buyers work with media agencies who work with DSPs, data providers/sellers, and verification vendors, who in turn work with SSPs, who work with publishers. Aka the “supply chain.” If the advertiser has replaced its media agency partner and taken all aspects of programmatic media in-house (tech contracts, process, and hands-on-keyboard staff), then the rest of the supply is still in play.

1. Demand-side Platforms (DSP)

In March, we started with just two DSPs, TradeDesk and Criteo. TradeDesk has generated 35% of total portfolio returns, while Criteo has only contributed 1.2% to total returns.

That said, we think the market underappreciates Criteo compared to TradeDesk due to the latter’s deep position with agencies. On a Return on Capital Employed (ROCE) basis, Criteo delivers the same return as TradeDesk but doesn’t get as much investor love, even though both companies have equal exposure to cookie reliance.

Flash forward to 2Q21 and we now have four new public DSPs taking up room in our portfolio: Viant (DSP), Zeta (ZETA), Tremor (TRMR), and Acuity (ATY).

All four stocks have slid since going public:

Viant is off –78% (ouch!)

Zeta is down –20%

Tremor shares have lost –3% since re-debuting on the public scene

Acuity has shed –23%

We think there is much more downside to come for these DSPs as they struggle to attract advertiser budgets to their server clusters. That means their marginal cost of production (e.g., producing served impressions) faces a severe floor, which puts big-time pressure on contribution margins.

2. Supply-side Platforms (SSP)

When we launched Quo Vadis, we had precisely 1.3 SSPs: Magnite and Roku (1.0 and 0.3 components, respectively).

Magnite is the biggest open-web SSP besides Google’s SSP, AdX. As you’ll see in a hot moment, as relatively large as Magnite is in the SSP universe, it is having a hard time delivering financial returns relative to all the other investment alternatives investors have at their disposal.

Our other inaugural SSP component is Roku. Roku generates roughly ⅔ of its revenue from streaming subscriptions and the other ⅓ from ad sales. Since we assume most of the ad sales flow through programmatic pipes (e.g., connections to DSPs including Dataxu, acquired by Roku in 2019), we don’t count Roku as a “programmatic pure-play,” even though it does rely on programmatic success in a material way.

Back in March, Magnite contributed a whopping 44% to our portfolio gains but has trended down to a 32% share in August (and shrinking). Over the same time period, Roku has steadily contributed 15%, give or take.

As far as SSP newbies go, we include three in our portfolio. Two are what NYT calls “clickbait” — Taboola (TBLA) and Outbrain (OB). The third SSP is Pubmatic (PUBM), a direct competitor to Magnite, albeit much smaller in revenue terms.

Interestingly, while Maginte’s net revenues are nearly 2x Pubmatic’s, Pubmatic generates 38% more EBITDA and had created much more free cash flow since 2018.

Sure, it might appear that PUBM does more with less — and maybe necessity is the mother of invention — but the explanation could also be much simpler. If we rely on Occam’s Law stating that the simplest explanation is usually the best one, then maybe Pubmatic is simply better at maximizing publisher take rates and other fees than Magnite.

Anywho… Pubmatic joined our portfolio club in December 2020 and has 2 quarters of earnings results under the bridge. The market is clearly not impressed. PUBM is off –61% since its March 1st high and has -9% since its IPO in December 2020.

Taboola and Outbrain

With only two months of performance and its first earnings result posted last week, Taboola stock is down 15% (based on its Aug 27 price). From our POV, we find it hard to believe that any advertiser — particularly premium brands, but also e-commerce direct response players —thinks this clickbait stuff actually generates advertising results. But that’s adtech for you. Quo Vadis suggests knowing what you’re into — and also what you’re in for — before suspending basic advertising principles and spending blindly.

Quote of the Day: "Build a system that even a fool can use, and only a fool will want to use it." — George Bernard Shaw

Last but not least, Outbrain went public just a few weeks ago in July. After reporting earnings earlier this week, the stock is off 15% since its IPO.

Rajan Roy discussed the most intriguing thing about these players in his Margins column called “Taboola, Outbrain and the Chum Supply Chain.”

“…I'm talking Taboola and Outbrain. Most of my work in media has been on subscriptions and branded content, so I've never played in the depths of ad-tech darkness. But, I spent seven years trading currency derivatives and am well versed in the art of arbitrage. This is what makes a "Related Content" module so intriguing for me.”

WARNING LABEL: The rest of Rajan’s post is not pretty. ⛔️⛔️⛔️🤢🤢🤢

3. Data / Verification Vendors

Let’s start with data providers. Liveramp was and still is the only pure data company component in our programmatic portfolio. The stock is up 74% based on our portfolio starting point in January 2018, with a respectable 2% contribution to overall gains.

Despite all the disruptions to the cookie-based ecosystem, Liveramp has a deep tech bench and many top advertisers + large agency clients. Quarter by quarter, RAMP seems to be finding ways to overcome cookie diversity (and inclusion). 😂

They didn’t call Brian Lesser the “billion-dollar man” at GroupM for nothing

In other data vendor news, Infosum closed a $65M Series B round on August 17. If we had to guess, we’d venture to bet Infosum’s CEO Brian Lesser will find the surest and fastest way to the finish line. Between going public via standard IPO (takes time to grow sufficient revenue) and raising a monster round to SPAC with some M&A mixed in, we’d bet more on the latter.

DoubleVerify and Integral Ad Science

As far as Verification Vendors go, we’ve had two IPOs so far this year. DoubleVerify (aka “DV” to industry folks) came onto the scene in April, and Integral Ad Science (aka IAS) joined the IPO party in June.

Alas, public markets have high expectations for adtech newbies. Despite 44% growth in total revenue in its Q2 results, DV is off 7% since its IPO and 29% off its July high of $47.

IAS is in the same boat. The company delivered 75% revenue growth in Q2 earnings, but the stock is down 2% since its recent IPO. More importantly, unlike DV, which climbed 30% above its IPO price, IAS has only trended downward since its IPO.

In other IAS news, they acquired Publica (connects SSPs to supposedly unique CTV inventory) for $220 million, which seems to take IAS from a neutral, non-hands-on-media-budget role to one where they are getting involved with media budgets. If so, you’d think a clear conflict of interest should arise. On the other hand, the digital ad ecosystem can also be viewed as a system of many conflicts, so it might not matter at all.

Media Buyer Tip

If you can get your hands on a good valuation model for DV or IAS, you’ll see a line called “Media Transactions Measured (MTM).” Armed with MTM information, you can calculate the average % take-rate, which will be around ~8%.

If 8% of ad budget seems expensive for these (vanity) services, that’s because it is.

For advertisers who hire consultants to study working media (e.g. a more detailed version of ISBA/PwC’s work in the UK), they’ll typically see verification fees at 2% to 4%. But if the true take-rate is 8%, that means some unobservant advertisers are probably paying well north of 10% and have no idea. If you’re going to blindly trust adtech sales pitches over and over again, the best we can do is point you to The Prince, “a prince who is not himself wise cannot be wisely advised” (Machiavelli).

What’s It Worth? Let’s say a large CPG or car company spends $100M/year on programmatic ads. If the martekers in charge happen falsely believe verification fees are 2% when they’re really 10%, then they are leaving tons of value on the table. At a 7% cost of capital, the savings are worth $114 million = [$100M in spend x 8% savings = $8M ➗ 7% cost of capital = $114 million in potential shareholder value creation].

4. Agencies

Sir Martin Sorrell’s new-age agency holding company (S4 Capital) has been a key component of our programmatic portfolio from the get-go. It was the only agency we included, simply because the underlying assets trade much more like an adtech company than a traditional agency.

What’s really nice for S4 Capital is its defensive/offensive position. If bad news hurts more traditional agencies, S4 benefits as an adtech play. If bad news hits adtech, S4 benefits as an agency on the sharp end of the spear.

S4 Capital’s share price is up 653% since going public in Sept 2018. With its new branding as Media.monk, unveiled a few weeks ago, we see more growth ahead.

In other agencies news

Our Quo Vadis agency portfolio started with five legacy holding companies (WPP, Publicis, IPG, Omnicom, and Dentsu) along with S4 Capital which we classify as a new age holding company with 100% digital asset. Starting in August, we added another new age player — London-based Next Fifteen Communications (NFC).

Together with S4 Capital, we call this group of two “Agency Power Plays.” Instead of having to execute endless restructuring and cost-cutting exercises like legacy holding companies do, these new agency groups have the advantage of starting from scratch. They are better equipped to build against fast-changing marketer needs in an always-on digital world.

Between the two power players, they generate 95% of the gains in our agency portfolio.

Amongst the slow-growth legacy companies mired in organic growth optics and endless new pitches that go end where they begin, IPG is the only bright spot contributing a respectable 11% of the gains since January 2018.

More Public Newcomers on the Way?

Innovid, a CTV ad serving company, is looking to IPO via SPAC merger at a $1.3 billion valuation.

BuzzFeed also announced plans to go public via SPAC, targeting a $1.5 billion valuation.

In March, InMobi was reportedly going public at a $15B valuation. In more recent news, it’s been rumored that InMobi is in talks to take Xandr/Appnexus off AT&T’s hands. From our purview, it will be very telling to see if AT&T sells the unit for less than the $1.6 billion it paid in 2018. With revenues reported at roughly $300-$380 million annually (and losses between $50-$90 million), it seems very likely to go for less than $1 billion.

Mediaocean, a backend advertising services and software company used by many media agencies is rumored to IPO at some point. One thing is for sure: Mediaocean’s top management team certainly looks well-prepped for prime time.

Vista Equity Partners acquired a majority stake in 2015.

Mediaocean acquired Paris-based media management software provider MBS in January 2020.

Data science and media technology company 4C Insights was acquired in July 2020 for $150 million. At the time, Mediaocean’s reported value was $2 billion.

Most recently, Mediaocean announced the acquisition of ad server company Flashtalking for $500 million.

If Mediaocean does go public at $2 billion, it will be right in the middle of the pack and probably do well thereafter with its current management chops.

Ask Us Anything (About Programmatic)

If you are confused about something, a bunch of other folks are probably confused about the same exact thing. So here’s a no-judgment way to learn more about the programmatic ad world. Ask us anything about the wide world of programmatic, and we’ll select a few questions to answer in our next newsletter.

Join Our Growing Quo Vadis Community

Was this email forwarded to you? Sign up for our monthly newsletter here.

Get Quo Vadis+

When you join our paid subscription, you get at least one new tool every month that will help you make better decisions about programmatic ad strategy.

Off-the-beaten-path models and analysis of publicly traded programmatic companies.

Frameworks to disentangle supply chain cost into radical transparency.

Practical campaign use cases for rapid testing and learning.

What’s your take on the Yahoo DSP and why it doesn’t get compared as much to Trade Desk and other top players ?

How would you rate technology plays such as Adslot (ADS:ASX) and Adveritas (AV1:ASX) in this space?