#49: MediaMath, The Aftermath

Dust has settled; Is it worth it?; Tips for management.

Reading Time: 9 puzzling minutes

In July we posted our view on the data provided in MediaMath’s bankruptcy filing and attempted to puzzle together what the company might go for at auction. We concluded:

At auction MediaMath’s remaining assets could be had for somewhere between $35 million and $70 million depending on the value of goodwill — whatever it might be.

As reported by Digiday, “Infillion is confirmed as MediaMath’s new owner” buying the assets for $22M. Digiday’s (Ronan Shields/Seb Joseph) reporting on this story along with Lara O’Reilly’s reporting at Insider has been excellent.

At the time, we split the estimated $35 million of non-goodwill value between Property, Plant, and Equipment (PP&E) at $17.5 million and Intangibles (e.g. intellectual property, brand recognition, reputation, relationships, etc.) at $17.5 million.

Clearly, goodwill on the books is worth zero. So, assuming Infillion valued PPE on the low end and only cared about the intangible assets as the ground floor to rebuild the business, our $17.5 million estimation came in reasonably close to reality.

Dust Has Settled

Before we jump into it, here’s a shout-out to Ciaran O’Kane from Exchange Wire and FirstPartyCapital who nailed in once again with this LinkedIn post.

“The MediaMath debacle seems to have descended into ad tech farce. Wouldn't clients have gone elsewhere? And what about the money owed? Do the numbers even add up? Just seems really messy deal and rehabilitation exercise.”

Now that we have more information we can try to piece together a new puzzle to see what Infillion has in mind and answer the question, “Do the numbers even add up?”

As imperfect as this kind of analysis might be we’ll give it go away.

Rule of Thumb: A model will never tell you if an investment makes sense. It can only tell you if an investment does not make sense. Infillion’s court filings give us a few clues to set our model:

Infillion’s financial model calls for ~$30 million in operating losses over the next three years.

The new owners will inject ~$40 million in working capital to fund the projected losses.

Management’s intention is to hire 155 staff by the close of its third year of operations.

Management has also estimated that “Over the first three years, we expect to spend around ~$445 million on traffic acquisition costs and another ~$102 million in other operating expenses” with a belief “that MediaMath will end up remitting over a billion dollars in inventory traffic, data fees, and hosting contracts over the next five years.”

All in all, these plug values suggest management is looking to have a break-even business between three and five years from now. That’s a helpful clue to constrain a model.

Downstroke

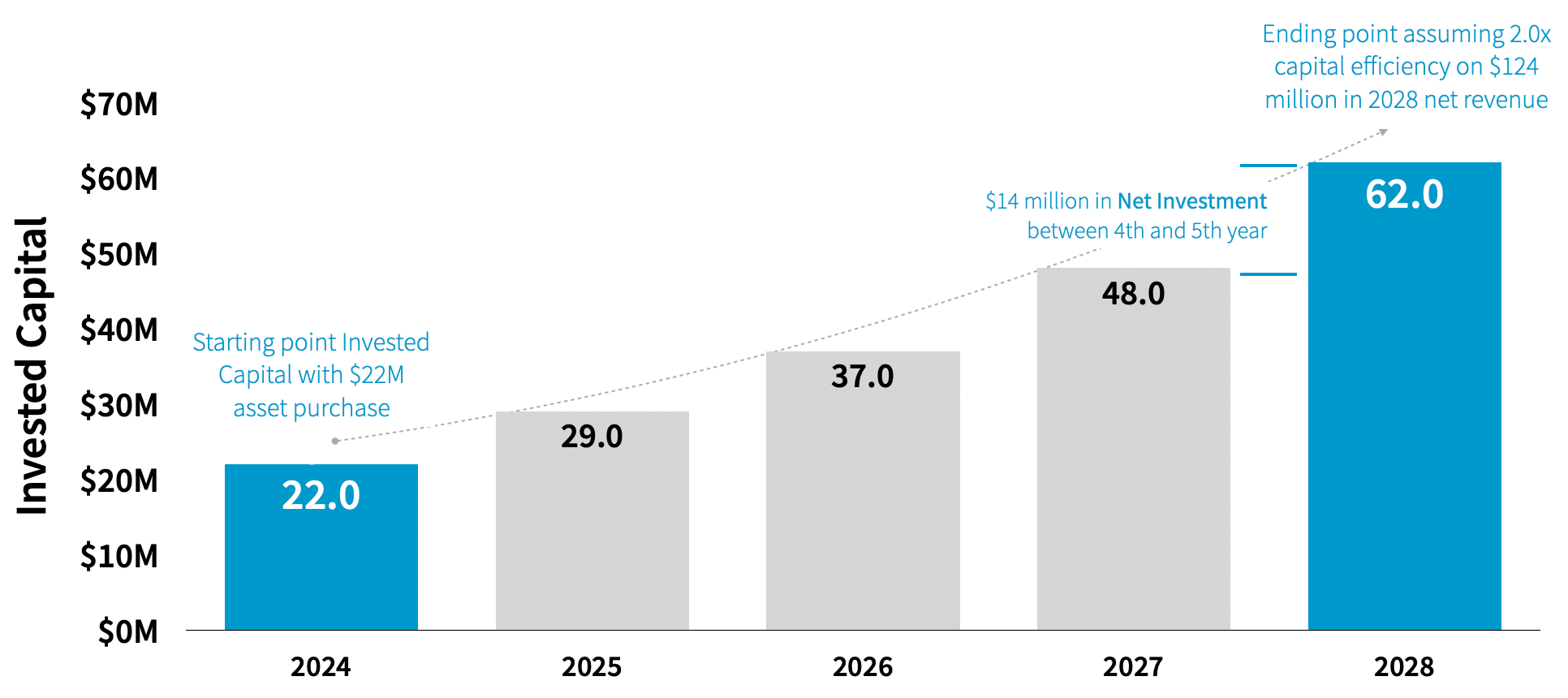

Infillion’s total investment is $62 million: $22 million for the assets plus $40 million in working capital cash to fund operations over the next three years.

Model Methodology

Our simplified model is a cash-out vs. cash-in discounted cash flow model. From what we can tell, Infillion is playing a hybrid venture capital/private equity role and looks at MediaMath as a re-started startup.

As such, we prime our model with how a VC/PE investor mindset would be looking to exit ~5 years down the road with a ~5.0x payoff. Therefore, with $62 million invested today (cash out), Infillion would be happy if the reborn MediaMath generates enough cash flow to be worth $310 million in 2028.

Net Revenue Five Years Down The Road

The Quo Vadis AdTechCore 10 players are currently trading at 5.4x net revenue. However, after we model out each company using favorable revenue growth rates AND assume meaningful cost reductions over the next five years (not easy to do, but A.I. will likely help if harnessed correctly) AND also assume good capital efficiency ratios (more on that below), we end up with an average adjusted net revenue multiple of 2.5x.

So, with a 2.5x net revenue multiple on an expected $310 million valuation down the road implied net revenue in 2028 is $124 million.

Take Rates & Gross Ad Spend

Trade Desk is the clear leader in the space with 20% consistent takes rates year after year. Since MediaMath will have to woo media agencies, marketers, and procurement into usage and retention, our model assumes a 15% take rate.

Therefore, $124 million net revenue on 15% take rates implies gross ad spend of $827 million running through MediaMath in 2028.

Operating Profits

Operating profits are hard to come by in AdTech Land. Looking at the QVAdTechCore10, only a few sniff 10% margins and several can’t find positive ground which is mostly due to high variable costs and high fixed costs (people).

That said, the programmatic adtech space is still relatively young. We can envision a future over the next few years where supply path optimization weeds out nonsense bidding inefficiencies and other redundancies bringing variable costs down. We can also envision AI-driven productivity gains reducing people-related costs.

Let’s assume everything goes well for MediaMath and set an ambitious operating profit target (EBIT) of 15% in five years’ time. With $124 million in net revenue and 15% operating margins, MediaMath’s new owners would generate $19 million in operating profit in 2028.

Taxes

Infillion management said they plan to have –$30 million in cumulative operating losses over the first three years. With that in mind, we assume MediaMath’s tax loss carryforwards will carry well into the future which means operating profits and net income are the same. Therefore, MediaMath’s Net Operating Profits AFTER Taxes (NOPAT) in 2028 would also be $19 million.

People Cost Ratios

Trade Desk’s variable costs (aka “platform operations”) are ~20% of net revenue. That’s a big cost to process data, crunch numbers and run servers. At the risk of being generous to MediaMath’s future, we assume management will have to get these costs down to ~10% of net revenue by 2028 ($12.4 million).

From here, we can impute $93 million in fixed operating costs (SG&A, R&D, etc.) five years in the future.

Net Revenue $124M

➖ Operating Profits $19M

➖ Variable Cost $12M

🟰 Fixed Operating Costs $93MWe assume people-related costs are ~70% of fixed costs like at other adtech companies ($65 million). Knowing that MediaMath’s monthly salary burn was $3 million + another $950,000 in payroll tax burden (see court filing motion), average employee costs are $245,000 per year. Given these values, MediaMath would employ 260 people in 2028.

Recall that management is targeting 155 people in Year 3 so we think our 260 value makes sense if growth goes as planned.

In our July 7 post, we showed that the average net revenue per employee across the QVAdTechCore10 is $400K. With 260 employees and $124 million in net revenue, MediaMath would be ahead of the game at $480K per employee. Trade Desk ran at $569K in net revenue per employee FY22.

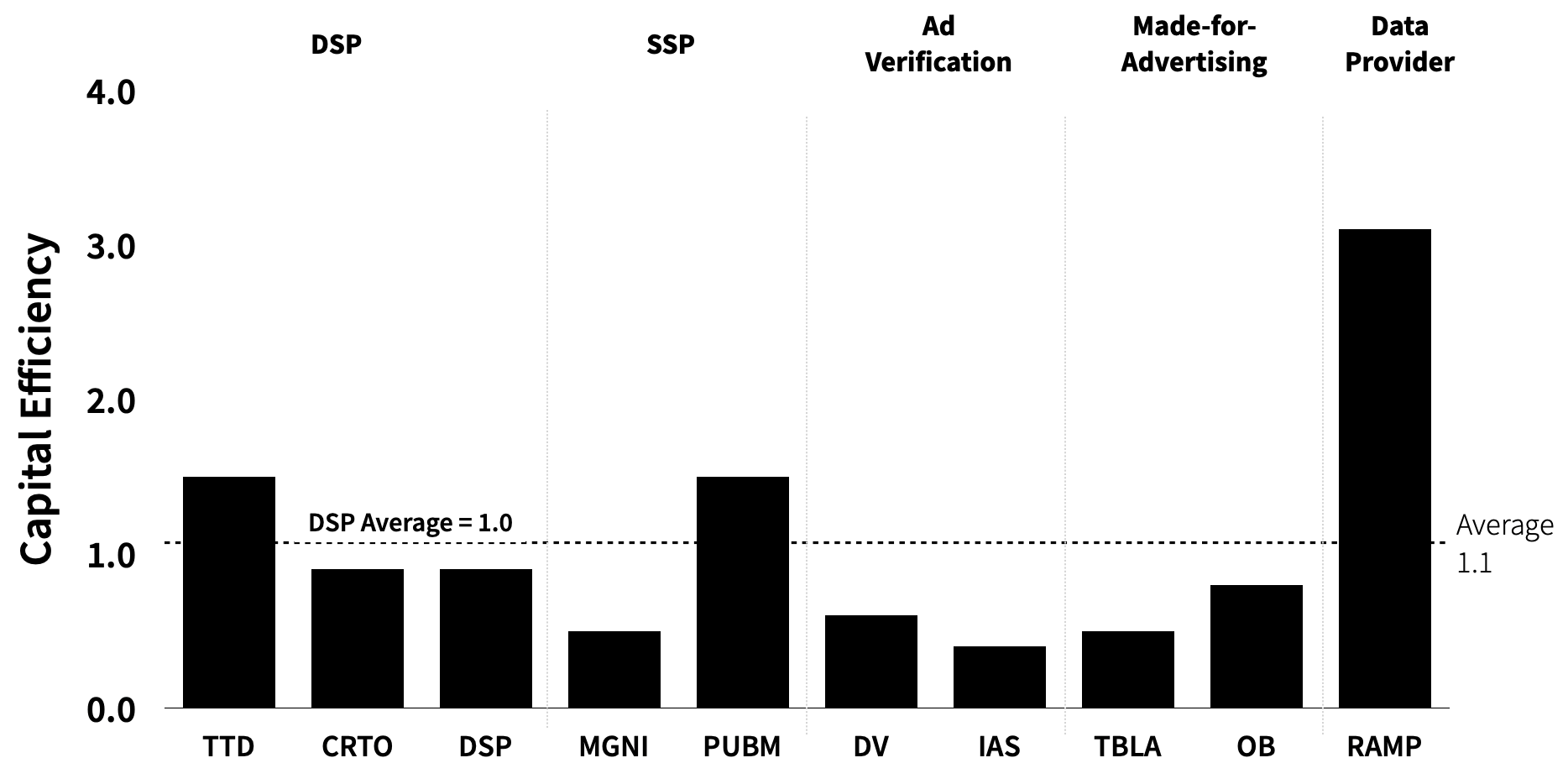

Capital Efficiency & Invested Capital

Now for the critical part. The QVAdTechCore10 generates $1.10 in net revenue for each dollar of invested capital. The three DSPs we track — TTD, CRTO, and DSP — average $1.00 in capital efficiency.

Let’s say the new MediaMath is incredibly well-managed and achieves 2.0x in capital efficiency in 2028. Since a large portion of invested capital is typically working capital, MediaMath management will want to re-build with a “collect-early-pay-late” mindset.

For example, if they can manage to collect in 45 days instead of 100 like other DSPs and pay SSPs (or publishers) directly in 60 days instead of ~100 days that would certainly help (see Digiday’s comments hinting how Joe Zawadski’s new company FXM could potentially help to fix working capital issues in the adtech space).

So, with $124 million in net revenue, we can back into projected invested capital at $62 million in 2028. With our $22 million invested capital starting point and our imputed $62 million value five years into the future, we can map out a curvilinear growth line to estimate net investment between the 4th and 5th year of operations which is $14 million.

Net Investment is the YoY change in invested capital which equals the change in working capital and capital expenditure.

Free Cash Flow In Year 5

With $19 million in NOPAT and $14 million in net investment in Year 5, MediaMath would generate $5 million in free cash flow.

NOPAT $19M

➖ Net Investment $14M

🟰 Free Cash Flow $5MWith $62 million in invested capital in 2028, management will have achieved a 30% return on invested capital (ROIC) which would be totally amazeballs!

Notably, there is not a single player in the QVAdTechCore10 that generates anything thing close to 30% ROIC. That’s coveted territory for the best-performing companies in the world.

Equity Value

Okay. So our model estimates that the new and improved MediaMath will have $5 million in free cash flow in 2028. To simplify future cash flows, the model targets 5th-year cash flows and works backward with cash flow capture assumptions to mimic a semi-smooth growth curve:

We assume zero free cash flow for the first two years

$2.5 million in Year 3 (50% of the 5th year)

$4.0 million of free cash flow in Year 4 (80% of 5th year)

After Year 5, we let free cash flow grow 10% per annum for another five years (generous assumption). Finally, we assume a standard 4% terminal growth rate forever into a steady state future after Year 10.

For the cost of capital, we assume zero debt on the books and use a plug value of 15% starting in 2024. The AdTechCore10 averages around 12% cost of capital with a few players above 13%. In essence, we’re adding a ~3% extra risk premium for the time being given MediaMath’s uncertain future in a highly competitive and commoditized environment. We take the cost of capital down to 12% over time which is favorable to valuation.

Gross Ad Spend and Supplier Payables

Let’s assume MediaMath manages to generate $14 million in first year (2024) net revenue on 15% take rates. That means MediaMath would have attracted or re-attracted $93 million in gross spend from advertiser clients and owe $79 million to suppliers.

Net Revenue $14M

➗ 15% Take Rates

🟰 Gross Ad Spend $93M

➖ Net Revenue $14M

🟰 Supplier Payables (SSPs, Data, etc.) $79MAchieving $93 million in clients should be doable with a few medium and small-sized advertisers or just one whale.

In the 5th year, we said gross ad spend on $124 million in net revenue and 15% take rates would be $827 million. That means payables to suppliers (mainly SSPs and data sellers) would be $703 million.

Referring back to one of Infillion’s clues — “Over the first three years, we expect to spend around ~$445 million on traffic acquisition costs” — our calculations trap this value to help tune and sanity check the model.

Valuation Result

Given everything we’ve covered and what we think are favorable assumptions compared to peers, MediaMath would be worth $56 million. With $62 million invested by Infillion and a $310 million target valuation at exit, the results of our model indicate a losing investment. It’s an uphill battle any way you cut it.

If we boost fifth-year operating margins from 15% to 25% and assume incredible capital efficiency of $3.00 in net revenue for every dollar of invested capital (instead of $2.00) with a terminal growth rate of 5% instead of 4% then we get to a $310 million valuation. Maybe it is doable, but it will not be easy.

Tips for Management

The number one objective in AdTech Land is to attract as much ad spend as possible. More is never enough. We recommend focusing on three areas. Although we make it sound easy it is really hard to pull off.

MediaMath is known to have solid tech but “they” say it is not easy to use compared to other DSPs. The Trade Desk (and Google’s DV360) is also known to have solid tech and folks say it is easy for campaign managers to use (mainly agencies). Making MediaMath’s platform easy peasy to use reduces friction to achieve customer buy-in. In other words, if they sell 6-minute abs you have to sell 5-minute abs. A great sign of momentum is when a business moves from outbound selling to inbound order-taking so management should be aiming strategy to somehow get there.

The fastest road to success in AdTech Land is to hitch yourself to a star and those stars are called media agencies. Incentives matter for agencies. Let’s face it, DSPs are commoditized machines and they all do the same thing more or less. The DSP that wins is the one that provides the best financial incentives and the one that makes agencies and marketers look good. Get there and now you’re order-taking.

That leads me to the third area. If Infillion can figure out how to collect early and pay SSPs late while reducing both receivables and payables from ~100 days to ~60 days that will certainly help. The current supply chain is made of sequential liabilities which means various players turn to receivables financing. The interest charges add up in a meaningful way and are ultimately passed on to advertisers in the form of higher media costs. If a value proposition can be sold in such that advertisers (or agencies) pay MediaMath early, then downstream payment flows turn into liberated money which could help fund agency incentives and/or include them in the action.

It will be tough sledding anyway you cut it. Good luck! Godspeed!

Ask Us Anything (About Programmatic)

If you are confused about something, a bunch of other folks are probably confused about the same exact thing. So here’s a no-judgment way to learn more about the programmatic ad world. Ask us anything about the wide world of programmatic, and we’ll select a few questions to answer in our next newsletter.

Join Our Growing Quo Vadis Community

Was this email forwarded to you? Sign up for our monthly newsletter here.

Get Quo Vadis+

When you join our paid subscription, you get at least one new tool every month that will help you make better decisions about programmatic ad strategy.

Off-the-beaten-path models and analysis of publicly traded programmatic companies.

Frameworks to disentangle supply chain cost into radical transparency.

Practical campaign use cases for rapid testing and learning.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.