#98: What If Google Opens Up YouTube Inventory?

Breaking down YouTube demand and supply; Impact and strategic value

If you’re a green shoot adtech company or adtech investor, then check out the AdTech Economic Forum London 2025 on February 6. It’s a pitch event with a twist. Our amazing featured speakers will take us down the investor continuum and then we’ll hear six amazing pitches from green shoot companies that form the antithesis of Joe’s quote.

Remi Lemonnier, co-founder of Scibids turned angel investor

Giovanni Strocchi, Venture Partner at Blacksheep MadTech Fund

Claire Houry, General Partner at Ventech

Sir Martin Sorrell, Executive Chairman at S4 Capital/Monks

What If Google Opens Up YouTube Inventory?

Across our thousands of wonderful subscribers, Quo Vadis gets a steady stream of interesting questions. One recent question worth further analysis is:

Advertisers can only buy YouTube ad inventory directly from Google. What would happen if Google made a strategic move to open up YouTube inventory to external DPSs?

That’s a great question. Let’s unpack it.

Before getting into any particular aspect of Google’s business lines, the first thing to understand about this amazing company is its history of making incredibly disciplined decisions about investing in the future to generate free cash flow for investors.

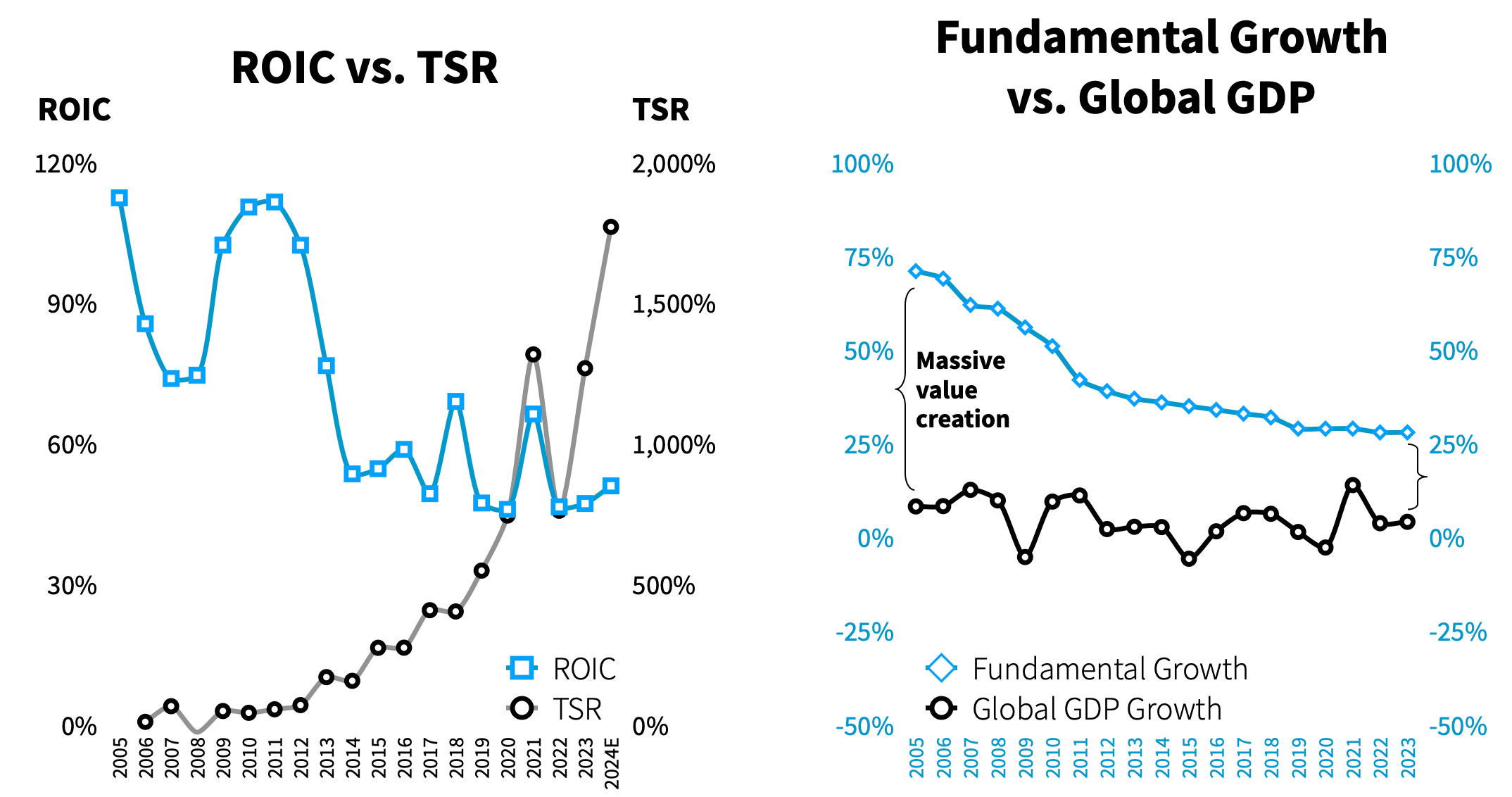

Since 2005, Google has generated an outstanding return on invested capital (ROIC) of 63%. Over time, it’s normal for ROIC to decline toward a steady state and move within a more predictable range. Google generated around 45% ROIC in each of the last two years. That’s way better than most. Given the first three quarters reported for 2024, we estimate 51% for FY24.

Looking at Total Shareholder Returns (TSR) since 2005, it’s natural for investors to reward companies that deliver high and consistent ROIC. Given stock price action over the last few months, the market is expecting even higher ROIC for FY24 (e.g. from 45% to 51%+).

Turning to the chart on the right, you can see that Google also delivers incredible fundamental growth, which is a function of the rate at which a company reinvests operating profits back into the business multiplied by its ROIC in the same period.

Over time as companies mature and industries settle into “perfect” competition, fundamental growth eventually regresses toward global GDP. Google is 26 years old and still growing at 7x the rate of global GDP. This is what happens when you either build or buy the best mousetrap.

Case and Point:

If Google decided to open up YouTube inventory to outside buying platforms, it would likely only do so if such a move directly drives or sustains high ROIC or indirectly drives more ROIC through strategic knock-on effects, which we’ll cover next.

Describing YouTube’s Supply Curve

Content Creation Drives Supply: YouTube's ad inventory is tied directly to the volume of video content uploaded by an estimated 3 million creators, of which there seems to be a near-infinite supply.

With millions of creators uploading videos daily, YouTube maintains a vast supply of ad slots, particularly in the form of pre-roll ads, mid-roll ads (inserted in longer videos), and post-roll ads. YouTube also monetizes banner-style ads that are shown alongside or on top of videos. Note that a similar incremental format is coming to CTV albeit modified to enhance large-screen experiences (see Olyzon.tv as a prime example).

In addition, the amount of YouTube ad inventory supply is also determined by the time users spend watching videos. More user engagement (time spent) drives more ad slots (supply). According to eMarketer, US adults spend 58 minutes daily on YouTube vs. 62 minutes on Netflix. Needless to say, the supply of YouTube inventory is robust and growing.

Describing YouTube’s Demand Curve

YouTube attracts advertisers from various industries due to its broad audience reach and high attention metrics. It also offers targeted ad placements based on demographics, interests, and behaviors.

Most importantly, advertisers demand YouTube inventory due to its exact targeting options across audience segments (e.g., age, gender, interests), contextual targeting (e.g., specific video categories), and retargeting (e.g. chasing high-intent shoppers).

Looking at eMarketer data on US YouTube ad spend, Google will generate around $17 billion in FY24 revenue (~$35 billion globally, roughly 48% US-based demand).

YouTube is bigger than all the other CTV players combined and gradually taking an increasing share of linear TV time as creator supply improves, diversifies, and grows. Again, if you build a better mousetrap the world will beat a path to your door.

Market Dynamics

YouTube operates on a real-time bidding system through Google Ads to connect supply with demand. In theory and likely in practice too, prices are determined by competition for ad slots and relevance.

Notably, advertisers cannot buy YouTube ads through external DSPs like The Trade Desk, Yahoo’s DSP, MediaMath, etc. The only way to access YouTube ad inventory is directly through the Google Ads platform or DV360 which are part of Google's proprietary advertising ecosystem.

Referring back to Google’s supreme ROIC performance, operating from a position of demand-side exclusivity is a strategic choice to maintain control over high-value/high-attention inventory (the means) and to maximize ROIC for its shareholders (the ends).

Again, if Google decided to open up access to more demand sources it would likely only do so if the probability of achieving or sustaining high ROIC outweighed any downside risk to one of the best businesses (if not the very best) in the ad world.

Playing It Out

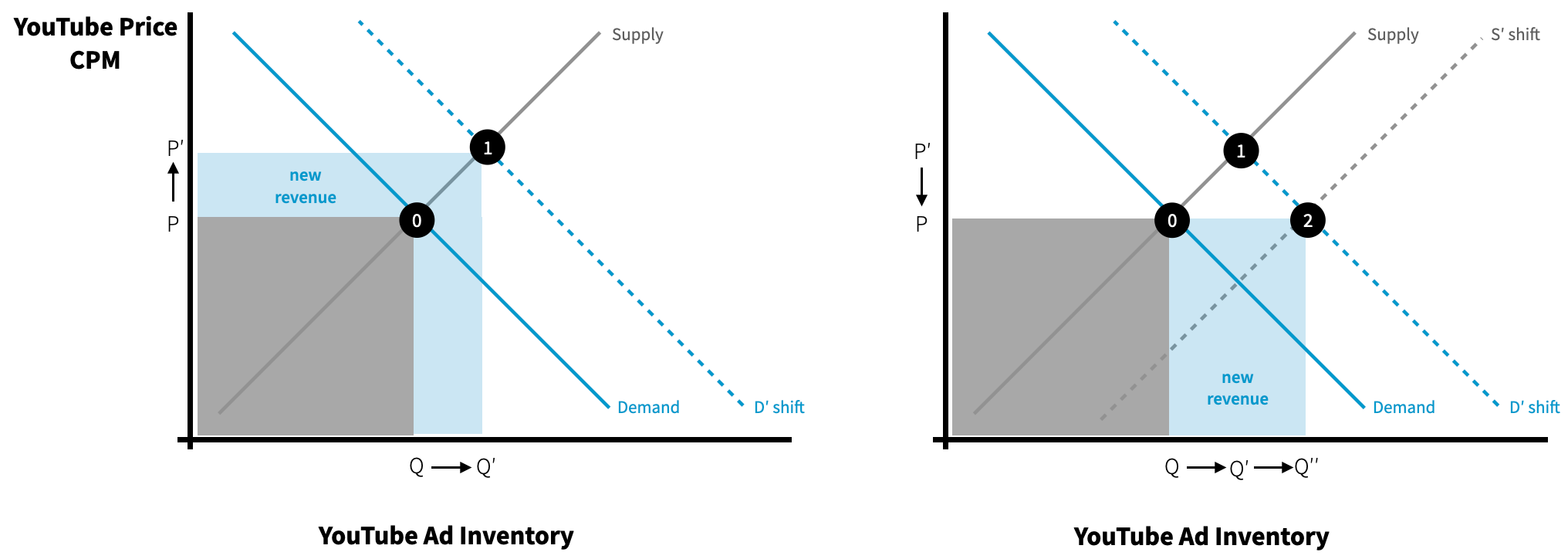

If Google were to open YouTube ad buying to other DSPs, the dynamics of demand and supply for YouTube inventory would shift significantly. Here's how this change might play out:

Increased Demand: Opening YouTube inventory to other DSPs would bring a wave of new buyers (e.g. advertisers using platforms like The Trade Desk). Many advertisers who currently avoid Google Ads or DV360 (due to platform limitations, data transparency concerns, or agency preferences) would now be able to access YouTube inventory increasing overall demand.

Starting with the chart on the left, one can imagine a material shift in demand from the current equilibrium to a new state with higher prices resulting in increased ad spend on YouTube (the light blue shaded area illustrates the incremental increase in market size).

Given auction dynamics, Google would earn more revenue than before while external platforms would earn buyer fees for facilitating the transaction. It’s a win-win-win for all parties: Google, external platforms, and advertiser choice.

Over the short run, the surge in demand would almost certainly result in higher costs per impression for advertisers, particularly for highly targeted or premium inventory. But over the medium term, it seems more than plausible that Google could expand YouTube ad inventory supply to match the demand shift thus bringing prices back to where they were before effectively selling more inventory at the old price but still generating incremental revenue or surplus value of which a portion is shared with external DSPs (see chart on the left side).

Another market benefit could come from DSPs with advanced targeting and optimization capabilities that might unlock value in inventory that Google Ads or DV360 underutilize today. This could improve overall yield on lower-quality inventory. Moreover, larger or more advanced DSPs like The Trade Desk would likely develop new tools and metrics for evaluating YouTube inventory thus increasing transparency and creating more competitive ad-buying strategies.

Other Knock-on Effects

Other platform players in the programmatic ad market would also benefit from such a policy change from Google. As more advertisers bring more ad dollars to YouTube ad inventory, they would likely lean on ad verification partners to provide additional services around viewability, brand safety, and attention metrics.

For example, public ad verifications like DoubleVerify and IAS, as well as private players Zefr and newer entrants like Scope3 with its recent acquisition of Adloox would all benefit in this refreshed competitive environment.

In theory, ad verification vendors can provide as many services as the market demands so the supply curve is basically horizontal. That means any shift in demand for these services will not increase prices but it will increase the quantity bought and sold resulting in more revenue for ad verification vendors.

Last but not least

During 2024 there was no shortage of negativity expressed by many adtech ecosystem players toward Google in the DOJ’s anti-trust cases (search and display ads business). Notably, Google’s YouTube business is not involved in either case.

From Google’s perspective, making a move to open up YouTube inventory to external platforms would demonstrate competitive friendliness and simultaneously send a strong signal about its openness to support a robust market with more buyer choices to access its world.

One can imagine how all the past ecosystem negativity would quickly change its tune from reprimand to praise with a simple win-win-win move. Both Google and many adtech players would gain incremental revenue with no material change to Google’s invested capital in YouTube thus directly increasing ROIC for shareholders. Such a move would also indirectly increase Google’s value on a risk-adjusted basis as DOJ litigation risk decreases and the economic spread between ROIC and cost of capital expands to new levels.

Have some fun and answer our poll question

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.

For me, they'll only open up as a fob to the regulators to stop more meaningful disposals. The revenue upside of opening up YT is negligible compared to the strategic impact on their AdTech ecosystem. Advertisers have to have a Google product today but not in an open world. Worth noting YT already stage the opening up of new placements/platforms/Geos etc to dampen the inflationary effects of increasing demand - eCPM payouts to creators only go down in the long run. Agree with Richard re: data access.

Tom, a few flaws in this piece IMHO -

1) it seems highly unlikely there are advertisers (Google would have the largest number alongside Meta) that would be brought incrementally to YT. I struggle to think TTD or Yahoo has a major buyer that does not also work w Google;

2) the value of YT inventory is intrinsically linked to the wider data Google collects on logged-in users (or infers probalistically where users are not logged-in), and draws upon Search history, location, etc. How could those other DSPs be competitive in "decisioning" without that data?

3) From a regulatory perspective, what need does Google have to open up, any more than any other FAST content provider is obliged to sell via agents?

4) Finally, you have not considered the downsides and costs of providing access to that inventory and the risk others "sniff the bidstream" just to compare pricing and likely value. Google would be giving away a lot for nothing guaranteed.