#59: Trade Desk... Investor Expectations Reset

Reading Time: 7 minutes where expectations meet reality

"The first rule of an investment is don't lose (money). And the second rule of an investment is don't forget the first rule. And that's all the rules there are."

– Warren Buffett

What’s Going On?

The Trade Desk reported Q3 earnings last week. Management beat on revenue and adjusted earnings-per-share but Q4 revenue guidance spooked investors into a sell-off pushing the stock down ~30% off its July high.

Here’s what’s scary. When Magnite disappointed investors after Q2 earnings last August its stock got pounded. MGNI hasn’t bounced back. Time will tell, but it looks like TTD has been able to keep investor enthusiasm for a quarter longer than MGNI. Now things are getting real as investors increasingly struggle to bridge what TTD needs to achieve over the coming years to justify the high expectations built into the current stock price.

What Does It Mean?

Quo Vadis breaks down the sell-off into two areas:

Unreal expectations coming home to roost

Fundamental valuation is getting more real

The first reason for the sell-off is about setting crazy high growth expectations in the minds of investors but not showing enough free cash flow creation to justify it. When you sell the dream, you have to deliver it or investors will eventually run out of patience.

Yes, we all know the holy trinity of CTV, retail media, and identity are the big growth drivers. And not just for TTD, but for the entire adtech sector. Competition for CTV inventory, retail media partnerships, and identity ownership are everywhere. TTD is not the only player in town.

Webinar Reminder: We doing a valuation on Yahoo this Thursday. Yahoo is privately held by private equity firm Apollo and is incredibly well positioned to compete not only in CTV, retail media, and identity but also in a few other areas of comparative advantage. Register here.

TTD’s investors have big expectations. Before the sell-off last week, investors had $37 billion worth of market cap expectations. Now they have cut expectations bringing TTD’s valuation down to $30 billion. Even at $30 billion, there is still a huge steep mountain to climb and the clock is ticking to show real wins in CTV, retail media, identity, and AI too.

Not only do investors expect these big wins to happen in a highly competitive environment, but they also expect TTD’s take rates to remain stable at ~20%. As if that’s not enough, investors are also looking for costs as a percentage of revenue to come down as top-line revenue grows well beyond TTD’s current trend line to create free cash flow.

Fundamental valuation is getting more real

Anytime investor expectations look like they will not be reached, they re-value their worldview and make decisions. Put another way, TTD’s Q3 results and full-year outlook made investors rethink about the future and they adjusted their valuation downward.

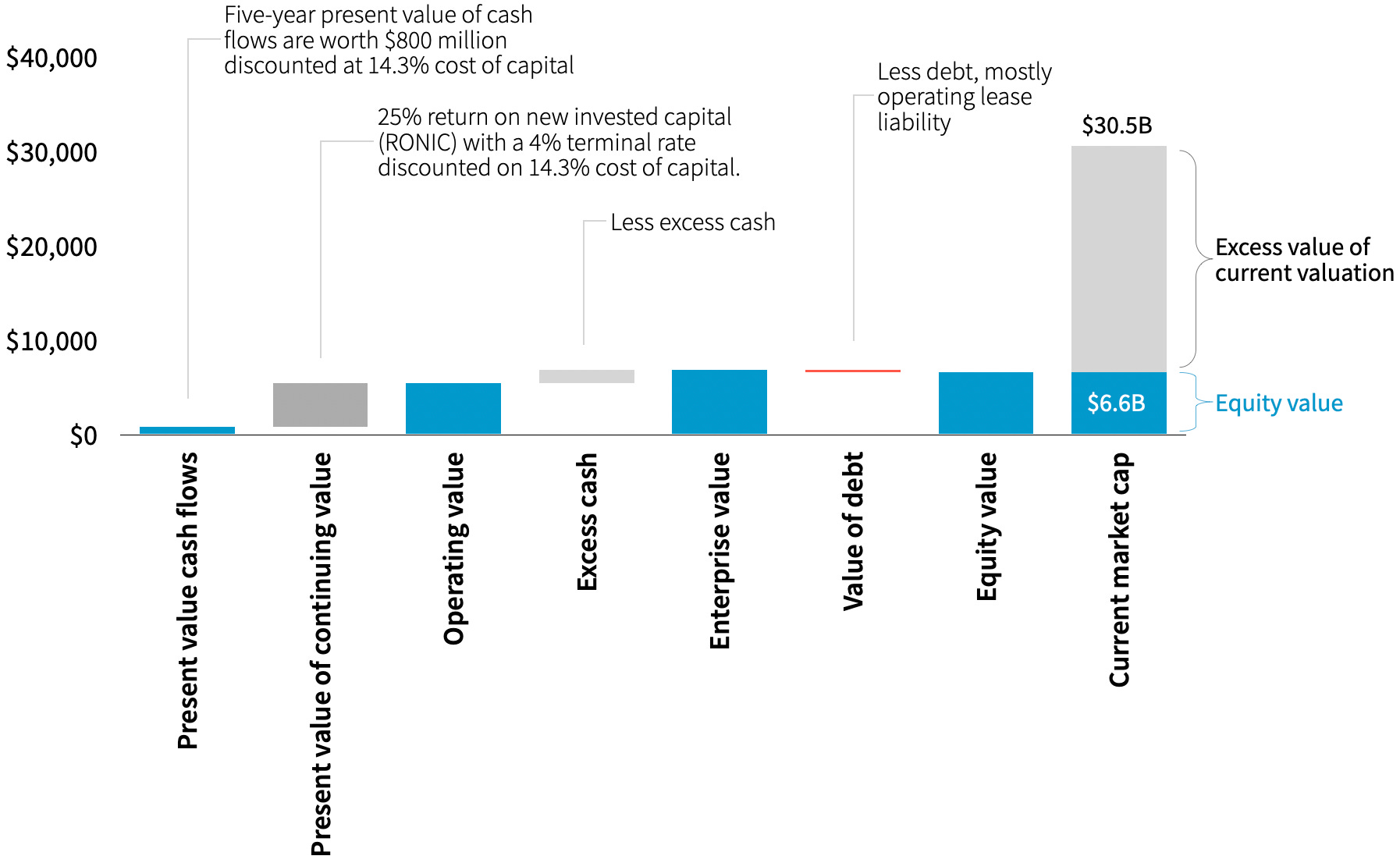

Let’s run through our valuation dashboard to see how things could shake out for TTD. In the end, our input assumptions will be incredibly favorable and we’ll arrive at a share value of ~$15.00 (the stock is trading at ~$64 today).

Revenue Growth

Like other adtech players, The Trade Desk’s net revenue growth since 2018 went up and down and up again through the pandemic years. Management guided to $580 million in Q4 against $610 million expectations pre-Q3 earnings. Quo Vadis estimates $600 million for Q4 resulting in $1.94 billion for the year and a 23% YoY growth rate.

With some benefit-of-doubt built into our model, we assume a 20% constant annual growth rate over our five-year forecast period. Our 20% growth assumption would beat the forward trend line by a wide margin resulting in $4.8 billion in net revenue in FY28. Assuming constant 20% take rates persist into the future, TTD will process $24 billion in gross spending in FY28 (gross ad spend was $7.7 billion in FY22).

Given management’s narrative around CTV and retail media as key growth drivers, this is where most of the growth will supposedly come from if everything goes to plan.

Operating Profit Margin (EBIT)

Operating profit margins are on a clear downward trend. On one hand, variable costs “platform operations” have improved since 2018 but fixed costs like SG&A and R&D have increased to 73% of net revenue in the recent quarter (note that stock-based compensation also sits within fixed operating costs).

Operating profit margins as a percentage of net revenue in Q3 were only 8.5%. Not that in 1Q23, TTD’s operating profit margin dipped into negative territory at –6.1%. In any case, our model assumes TTD will generate 8.5% margins for FY23 if all goes well in Q4.

Going forward to FY28, our model grows TTD’s operating profit margin to 25% on a straight-line basis. Make no mistake, that would be an outstanding performance. We assume continued improvement in variable cost unit economics (e.g. economies of scale from supply path optimization and efficiency gains in data crunching costs). We also assume AI and other productivity enhancements will help bring fixed costs down as a percentage of net revenue.

Needless to say, getting operating margins up to 25% of net revenue will not be easy and an amazing achievement if management pulls it off.

Net Operating Profit After Tax (NOPAT)

NOPAT is simply operating profits (EBIT) after cash taxes are paid to the government. We assume a 26% cash tax rate (21% federal marginal tax rate plus 5% for state and local taxes).

With net revenue growing at a constant 20% rate over the next five years with operating margins growing from 8.5% in FY23 to 25% in FY28, The Trade Desk’s NOPAT will gradually expand to nearly $900 million in FY28.

Notably, the NOPAT growth rate will be 38% in FY28. Again, that would be an astounding achievement. We’ll come back to this topic in a minute when we get to TTD’s continuing value.

Invested Capital & Net Investment

TTD’s invested capital has been growing over time albeit on a decelerating basis. On one hand, investors would probably like to see management re-invest more operating profits back into operating assets that drive growth. On the other, when a giant portion of revenue is eaten up by stock-based compensation and other expenses there is only so much cash to go around.

ROIC, Invested Capital Growth, and Capital Efficiency

With historical NOPAT margins in the mid-single digits (not stellar) and relatively little investment in new invested capital, TTD’s Return on Invested Capital (ROIC) was just 8.2% in FY22 and we estimate 10.7% in FY23.

That’s not great. In fact, in pure fundamental valuation terms, it’s value-destructive. We estimate TTD’s current cost of capital at 14.3%. With ROIC well below the cost of capital, the company is effectively destroying value for shareholders. Things might improve in the future, but that past performance is what it is.

In terms of capital efficiency — defined as net revenue generated for every $1.00 in invested capital — management has been improving this key value driver since 2018. Capital efficiency has expanded as net revenue grows on a relatively slow-growing invested capital base.

Assuming a constant 15% growth rate in new invested capital through FY28, capital efficiency will continue to improve from $1.70 in FY23E to $2.10 in FY28. Said another way, our model assumes TTD will grow invested capital by 15% each year over the next five years. Invested capital grew by 12.2% in FY22, we estimate 11.9% for FY23.

Given the forecasted NOPAT growth discussed above and a 15% invested capital growth rate, TTD would achieve an ROIC of nearly 40% in FY28. Again, that would be a stellar performance.

Free Cash Flow (FCF)

With 20% constant net revenue growth rates over the next years and growing operating margins to 25% with a 15% invested capital growth rate, The Trade Desk’s free cash flow will expand from what has been a negative story to a story of expansion and value creation.

However, even with all the favorability included in our assumptions, none of what you just read is nearly enough to justify the current stock price.

TTD Valuation Build-Up

Let’s summarize:

We’re growing net revenue at 20% per year over the next five years. That not only beats TTD’s trend line but it’s also ~2x market growth

Management finds ways to expand operating profits from 8.5% to 25%

We’re growing invested capital at a 15% constant rate over the next five years

We’re discounting free cash flow at a 14.3% cost of capital

The Trade Desk is currently trading at a ~$30 billion valuation. We just showed you a model breakdown with very favorable assumptions and only got a $6.6 billion valuation. That’s $13.50/share vs $62/share today.

Getting $62/share takes a big leap of faith as far as we can tell. Imagine the following:

45% revenue YoY growth rates into the future with take rates remaining at 20%

50% operating profit margins

Just 5% YoY growth in invested capital

What are the chances of that happening?

Back to where we started

Management has set super high expectations in the investor’s mind. When investors recalibrate the chances of achieving these mighty expectations they will tend to re-value the company downward again and again until the probabilities level out. That’s are read on what happened to TTD after Q3 earnings.

How wrong could be and how much might it change our answer?

Technical Notes

Free cash flow is defined as NOPAT minus net investment in invested capital

Net investment is inclusive of depreciation add-back

Invested capital is defined as operating assets minus non-debt operating current liabilities minus excess cash

Excess cash is defined as total cash and equivalents minis operating cash (4% of net revenue)

Share price is calculated using total common shares outstanding to account for stock-based compensation being treated as an expense.

Ask Us Anything (About Programmatic)

If you are confused about something, a bunch of other folks are probably confused about the same exact thing. So here’s a no-judgment way to learn more about the programmatic ad world. Ask us anything about the wide world of programmatic, and we’ll select a few questions to answer in our next newsletter.

Join Our Growing Quo Vadis Community

Was this email forwarded to you? Sign up for our monthly newsletter here.

Get Quo Vadis+

When you join our paid subscription, you get at least one new tool every month that will help you make better decisions about programmatic ad strategy.

Off-the-beaten-path models and analysis of publicly traded programmatic companies.

Frameworks to disentangle supply chain cost into radical transparency.

Practical campaign use cases for rapid testing and learning.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.