#25: TradeDesk Take-Rate, and More

Deep Dive; Ad Flow Multiples; Sum-of-Parts Revenue Analysis

Reading Time: 13 fruitful minutes.

Today we celebrate National Hug a Newsperson Day. Hold me! We’re both going to need it after the next 13 minutes in Programmatic Land.

For Quo Vadis+ subscribers, you can access the model for this post here.

Digging into The Trade Desk’s Ad Flows and Margins

In 1998, Bill Clinton gave the best non-answer of all time:

“It depends on what the meaning of the word "is" is… if "is" means is and never has been that is not – that is one thing. If it means there is none, that was a completely true statement. But, as I have testified, and I'd like to testify again, this is – it is somewhat unusual…”

When “it” comes to breaking down how The Trade Desk (or any DSP) earns its fees, it all depends on the word “it.” Allow us to explain.

In the world of economics, there are two broad schools of thought: Positive Economics and Normative Economics.

Positive Economics studies why things actually are in reality.

Normative Economics is more about how things should be or could be.

Our observations of The Trade Desk’s margin-making ability fall into the normative bucket. While our analysis is by no means a certainty, we do know enough about programmatic to at least express an idea and framework of what it could be.

With our econ hats on, we don’t really care about the size of any programmatic actor’s margins. The more the merrier, as they say. That’s the whole point of being in business, after all, and one good reason why investors make investment choices.

From an advertiser’s point of view, they probably would like to know more about how DSPs make money off their ad budgets, but there is no observable certainty of that kind of deep curiosity in Programmatic Land. And that probably explains more than enough about chronic transparency concerns around all the many fees big and small.

The Trade Desk’s 2021 Performance Was Totally Outstanding

We tip our Quo Vadis hats to TTD’s management team, which is clearly among the best in Programmatic Land.

Revenue and profit growth in 2021 were by far the best across the programmatic stocks that we track.

With invested capital hovering around $1 billion and Net Operating Profit After Taxes (NOPAT) at $124 million, TTD is one of our best ROIC producers (Return on Invested Capital) at a respectable ~13.5%. Getting ROIC above the rising cost of capital for adtech players, let alone into positive territory at all, is tricky in this $70B+ sector of global media action.

ROIC 101: Let’s say you have a mortgage on your house and pay 3% interest on your loan. Let’s also say your effective income tax rate is 25%. You get to write off the interest portion of your loan when you do your taxes, so your real cost of debt is 2.25% [3% x (1-25% tax rate)]. Since you own 100% of your home, your cost of debt represents your entire cost of capital. If your abode appreciates 5% annually, your ROIC is above your cost of capital which means you created real cash value.

With a whopping $6.2B in ad flows under management, TTD grew its ad budget attractiveness by 48% YoY. How in the world did they do it?

Part of it is undoubtedly thanks to a well-trained and well-incentivized sales team.

A good chunk is due to parking themselves right next to the firehose of agency buyers who control the biggest portion of an $836B media market—particularly across the Fortune 500, who collectively generate $33 trillion in revenue. Where there is revenue, there is ad budget looking for a home.

Another explanation is an ability to take on managed service work from overloaded and understaffed agencies. The money has to go somewhere. It usually flows toward the path of least resistance, which is toward human labor that pushes keyboard buttons to make sure the money gets spent.

Another big growth driver for TTD as the second biggest DSP behind Google is also thanks to Google itself. When CMOs and their staff read about auction-rigging tomfoolery like “Project Bernanke” in the Wall Street Journal, they tend to look for the next-best alternative. That’s always a great spot to occupy in the ever-volatile media space.

Last but certainly not least, it took years of hard work to win that coveted position in a highly competitive market. That should tell investors something about how good TTD’s management team really is.

The least likely factors are probably technology, data prowess, and supply. After all, buyers can get that anywhere.

Advertiser Cost or Media Cost-Based Take-Rates for Trade Desk?

With $6.2 billion in ad budget flowing through TTD and $1.2 billion in net revenue extraction, TTD’s implied take-rate is 19%. These two numbers are by far the most important for investors because they drive the most important outcome: ROIC and value creation. Investors want to know how good an adtech company is at attracting ad flows, and when they do, how good are they at extracting fees.

For TTD specifically, more ad flows drive more negotiating power with sellers — this is probably why TTD launched OpenPath to source inventory directly from publishers.

More ad flow allows for more margin-making creativity and for more options to prevail.

And most importantly, more ad flow volume drives down the variable cost of crunching data and running intense QPS compute cycles, thereby allowing bigger players to be the most price-competitive.

Comparative example of the only two DSPs that disclose ad flow data

TTD has a market cap of $30B and trades at ~5x ad flows with 19% reported take-rate margins.

Criteo only trades at less than 1x ad flows with a market cap of just $1.7B on a 40% take-rate (gross margin), but CRTO also produced 21% higher earnings (EBIT) than TTD in 2021. Go figure.

What explains the investor disconnect?

Well, investors know that pretty much 100% of Criteo’s revenues are manage-serviced by Criteo staff. Investors don’t like this as much as SaaS tech models, so it appears they value Criteo similarly to an agency model, which is also people-dependent. However, what investors may not know or fully appreciate from a valuation perspective is to what degree TTD is also dependent on taking in managed-service ad budgets from overburdened agencies like the rest of the sector.

If there is one thing that is true about the media business, and generally underappreciated, is the manual nature of how everything gets done in a cascading chain of outsourced labor.

FOFO Tip For Advertisers Looking for Transparency: Ask your media agency for all the names of the hands-on-key people who touch your campaigns in DSPs. Ask for their LinkedIn profiles too. Then ask to meet them every week for a 15-minute video call to teach you about what they do in bits and pieces. Doesn’t that seem like a fair and super easy ask. It really doesn’t get any easier if you want gain an outsized impact on your own programmatic knowledge. It’s so easy that if a marketer doesn’t care to ask, then at least they know they suffer from FOFO — the root of all bad future decisions but probably really great for adtech and investors!

Breaking Down TTD’s 19% Take-Rate

With $6.2B in ad flows running through its programmatic pipes (minus $1.2B in fees), TTD’s take-rate is 19%.

What Quo Vadis readers would probably like to understand is how this $6.2B in ad flows is defined. Specifically, how is the $6.2 billion in the denominator defined? We know TTD defines it as “total spend on our platform,” but what does that really mean? Well, “it” all depends on what “it” is.

Let’s take a look at TTD take-rates through the positive lens of how things could be. By piecing together what we know about DSP internal accounting functions and other observable information floating around Programmatic Land, we can see how things could be. We’re interested in forming the question in case anyone in our Quo Vadis community wants to ask about it.

TTD Take-Rate Break Down

Let’s take it one step at a time.

$6.2B in advertiser demand coming into TTD is mostly through the hands of media agencies.

TTD calls it “total spend on our platform.”

Quo Vadis calls it “Ad Flows.”

For all you hands-on-keyboard folks out there in Programmatic Land, what we call Ad Flows is typically called “Advertiser Cost” in DSP reporting platforms.

What matters most is that once the $6.2B hits TTD, that’s all there is for TTD and other integrated players to work with.

Other adtech people’s money

All downstream fees must come out of ad flows. For instance:

Agency Trading Desk staffers will fill in a campaign setup field in the DSP to account for their services

Audience data fees also need to be deducted, which are likely sourced from Trade Desk’s “data from 130 data providers” or potentially Trade Desk’s owned and operated data assets.

Ad Serving fees so marketers can track impressions (usually Google Campaign Manager).

Content Verification services such as IAS or DV also need to be deducted from the $6.2B before TTD can make a single auction bid.

TTD calls out pre-bid revenue recognition accounting stuff in their 10K

10K-2021, Page 46: “We report revenue net of amounts we pay suppliers for the cost of advertising inventory, third-party data, and other add-on features (collectively, “Supplier Features”). Judgment is required to determine whether we are the principal and report revenue on a gross basis for Supplier Features or the agent and report revenue on a net basis for the amount of platform fees charged to the client. In this assessment, we consider if we obtain control of the specified service before it is transferred to the client, as well as other indicators such as the party primarily responsible for fulfillment, inventory risk, and discretion in establishing price.”

So, let’s say all those fees total 30% out of $6.2B.

Trading Desk @10% = $620M

Audience Data @10% = $620M

Ad Serving @10% = $310M

Verification @10% = $310M

That means around $1.9B in before-auction fees is deducted from ad flows by the DSP's internal accounting system.

You can think of this $1.9B as “other adtech people’s money.” Aside from volume-based discount deals on the back end, a DSP will have no claim on these funds.

Since DSPs are typically “integrated” with these four supply chain players, everyone collects log data to know who owes how much to whom. At some point, the advertiser or the media agency will get an invoice to pay these players.

Media Cost

That leaves $4.3B in what marketers have been programmed to understand as “Media Cost.” This is the money left over right before an auction happens.

We’re not at the auction block quite yet. Let’s assume DSPs like The Trade Desk charge around 10% in what adtechies call “tech fees.” This is basically like collecting rent to process bids for advertisers.

Assuming DSPs like TTD “take” around 10% of media cost, which is a reasonable estimate, TTD earns $430M in tech fees. This amount also needs to be deducted before any bidding begins.

Available Auction Funds

With all those fees finally out of the way, $3.9B remains in what Quo Vadis calls Available Auction Funds.

Auction Time

Now the bidding (and other things) begin. After the money is spent, we’d guess around $3.7B clears in the auction.

Hold on a second! What accounts for the $170M difference between what you went to auction with and what was actually spent?

Assuming TTD (or any DSP) is just like any other profit-seeking business, they must find a way to pass variable costs into the prices or fees buyers pay. Otherwise, profits are not possible. TTD calls these variable costs “Platform Operations,” which were $221 million in 2021 or 3.65% of $6.2B in ad flows.

10K-2021, Page 40: Platform operations expense consists of expenses related to hosting our platform, which includes “internet traffic” associated with the viewing of available impressions or queries per second (“QPS”), and providing support to our clients. Platform operations expense includes hosting costs, personnel costs, and amortization of acquired technology, and capitalized software costs for the development of our platform.

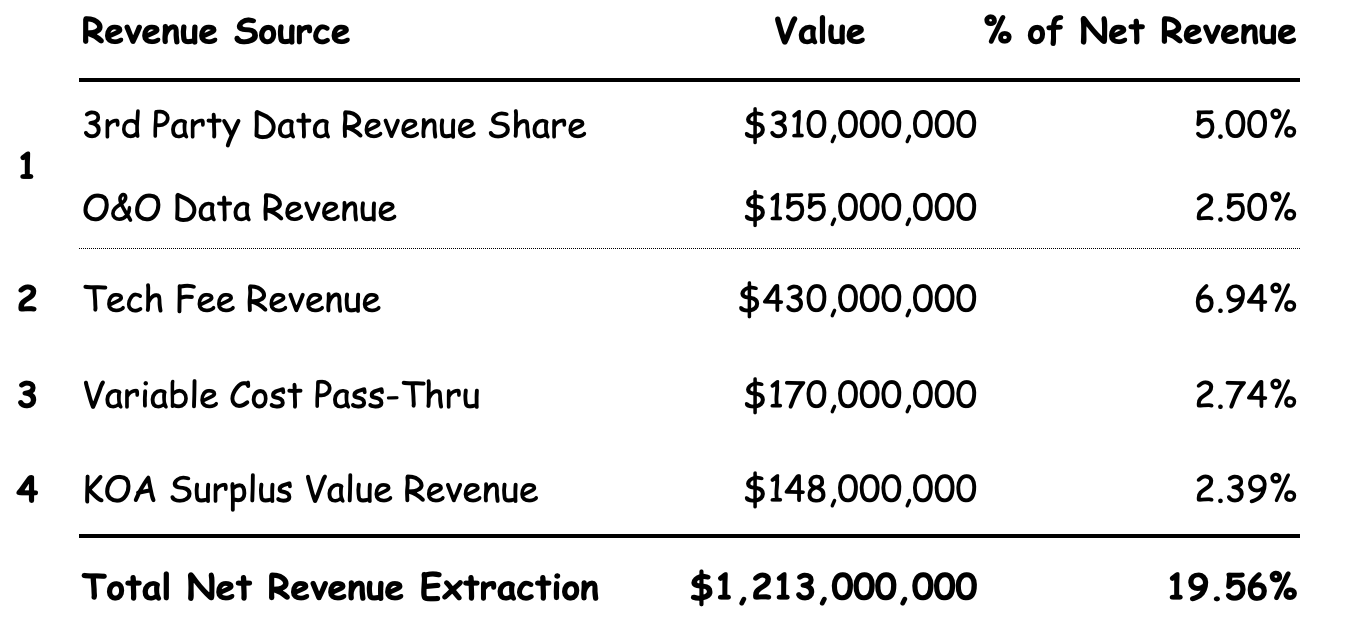

Revenue Extraction Sum-of-Parts

1. Audience Targeting Revenue (estimated $465M)

A good rule of thumb to estimate the audience data cost for your average large advertiser is around 10% of ad budget. So, with $6.2B in ad budget making its way to TTD, $620 million is used to buy audience data.

Trade Desk lists 110 third-party data providers in its data marketplace. In most cases, DSPs have revenue-share deals with these data partners. We think it is reasonable to assume a 50/50 split is a fair and mutually beneficial deal. If so, then TTD’s data partner revenue share comes to $310 million.

While nobody except for the DSP and their data partner knows how much data prices are marked up, some good advice for curious advertisers or investors is to simply ask. Best-case scenario, you get a decent answer and learn something. Worst-case scenario you get an answer like “We can’t disclose those terms due to confidentiality.”

But what about the other $310 million in advertiser data buys? The key question here is knowing how much of “it” is owned and operated (O&O) data sold by TTD as a principal trader. For a profit-seeking business, it seems reasonable that a DSP with good data products would want to maximize its O&O share and maximize margins.

If TTD sells 50% of the remaining $310M, then they would pocket another $155M in additional data revenue for $465M in total data revenue.

2. DSP Tech Fees (estimated $430M)

With $4.3B making its way to media cost, assuming a 10% average tech fee across all 980 customers (mostly agencies, see 2021 10K, Page 8), TTD generates $430M off the media cost reported in its platform.

3. Variable Cost Pass-Thru Revenue (estimated $170M)

Let’s say I sell you an apple for $1.00. Tucked away in that $1.00 is my variable cost of $0.50, aka the cost of goods sold (COGS). In DSP Land, you might know it as “carrying cost.” It’s probably an expressed contract somewhere in your DSP.

As an apple retailer, I buy apples from a farmer for $0.50 and sell one to you for $1.00, resulting in gross revenue. After we do the deal, I immediately expense $0.50 in COGS, resulting in $0.50 in net revenue. In other words, I pass my COGS expense on to you in the price you pay and then expense it. If I sold you an apple for just $0.50, I’d starve to death. So I’d eat the apple instead of selling it to you.

In DSP Land, variable cost pass-thru charges are most likely based on whatever the clearing price is, but nobody really wants to talk about that.

Anyhow, assuming a 3.56% carrying cost for TTD, they extract $170M in revenue and then expense it as any profit-seeking business would do.

4. KOA A.I.

Besides audience data and DSP fees, The Trade Desk has another smart revenue extraction strategy to support its take-rate. It’s called KOA.

KOA: Uses machine learning to find media savings through a tactic called bid shading. As publishers and exchanges have switched to first-price auctions in an effort to increase yield through tactics like dynamic floor pricing, buyers need to be careful not to overbid, as they might still be in a “second-price auction” (what a messy auction system)!

KOA basically tries to figure out seller price floors and how to lower first-price bids but still win the auction. Doing this successfully generates what economists call surplus-value. According to TTD, KOA reduces bid prices by 20% and keeps 20% of this surplus-value.

So, if $3.7B clears in auctions, then without KOA running, 20% more would have cleared ($4.44B) on the higher winning bid prices. That means KOA generated around $740M in surplus-value in 2021. Since TTD keeps 20%, they make an extra $170M in additional revenue extraction.

And that is exactly what you want to do. Attract ad flows and take as much as your customers will bear.

Understanding Real Take-Rates From the Advertiser’s POV

What advertisers should want to know to reprogram their programmatic mindset is the actual cost of media compared to the clearing price. If “it” is not the “media cost” reported by DSP platforms, then it must be something else.

The gap between media cost reported in DSP platforms and actual clearing price cost can be meaningful. The less you’re looking, the wider it probably is.

If $3.7B clears in auctions and you add back $465M in data revenues extracted before the auction to normalize the denominator, then the effective take-rates on a total net revenue extraction of $1.2B would be 29%.

Research Coffee Break — If you want to know more about variable cost pass-thru and get a detailed view of how DSPs deduct supply chain fees in order to determine how much is left over for bidding action, then check out this research paper.

Ask Us Anything (About Programmatic)

If you are confused about something, a bunch of other folks are probably confused about the same exact thing. So here’s a no-judgment way to learn more about the programmatic ad world. Ask us anything about the wide world of programmatic, and we’ll select a few questions to answer in our next newsletter.

Join Our Growing Quo Vadis Community

Was this email forwarded to you? Sign up for our monthly newsletter here.

Get Quo Vadis+

When you join our paid subscription, you get at least one new tool every month that will help you make better decisions about programmatic ad strategy.

Off-the-beaten-path models and analysis of publicly traded programmatic companies.

Frameworks to disentangle supply chain cost into radical transparency.

Practical campaign use cases for rapid testing and learning.

Thanks Jeff — it was not meant to be all-inclusive. It was meant to show that unaudited numbers like gross ad spend can be used to hide/manipulate other forms of take rate.

This is missing many fees like bid shading fees, mark up on data, api fees, deal library fees, etc.