#139: Liftoff IPO Valuation

Plausible, Possible or Probable?

Housekeeping

Last Media Dollar “Live” is coming to NYC: February 25, 2026. Last Media Dollar “Live” is coming to New York City on February 25 at the Roxy Cinema in Tribeca. This is not a panel, it’s a live, on-stage decision-making experience where senior practitioners and the audience debate assumptions and reveal how media choices are actually made under real constraints, in real time. Seats are very limited and moving quickly. Secure your ticket now if you want to be in the room where the thinking happens.

Advertising Economic Forum Returns to New York City: March 18–19, 2026.

This year features an expanded two-day format focused on where media capital, ad innovation, and financial strategy are heading. Day 1 at Horizon Media features eight AI founder pitches to our investor panel with live debate across agentic commerce, creative, and emerging agency models. Day 2 at The New York Times Center convenes 400 senior leaders for closed-door sessions examining market structure, incentives, and the economic forces reshaping advertising. Early bird registration is still open for now; space is limited.

Liftoff IPO Valuation

As reported by Reuters last Tuesday:

Liftoff, a mobile app marketing provider backed by Blackstone, filed for an IPO on the NASDAW under the symbol “LFTO”. Reuters reported last year that Blackstone was exploring a sale of Liftoff that could value the business at $4 billion or more, including an IPO or a private sale. The company intends to use IPO proceeds for general corporate purposes and to repay $1.8 billion in outstanding debt.

Rather than anchor on the rumored $4B value, let’s instead triangulate it from fundamentals with a simplified discounted cash flow approach starting with revenue and margin structure, and then turn to investment capital, optimistic forecast assumptions, and what it all implies to arrive at a fair equity value. If you’re into TLDR, after we assess past performance and plug in optimistic forecast drivers, we get to $3.1B in equity value. That said, we have a feeling the IPO will likely trade higher than our estimate.

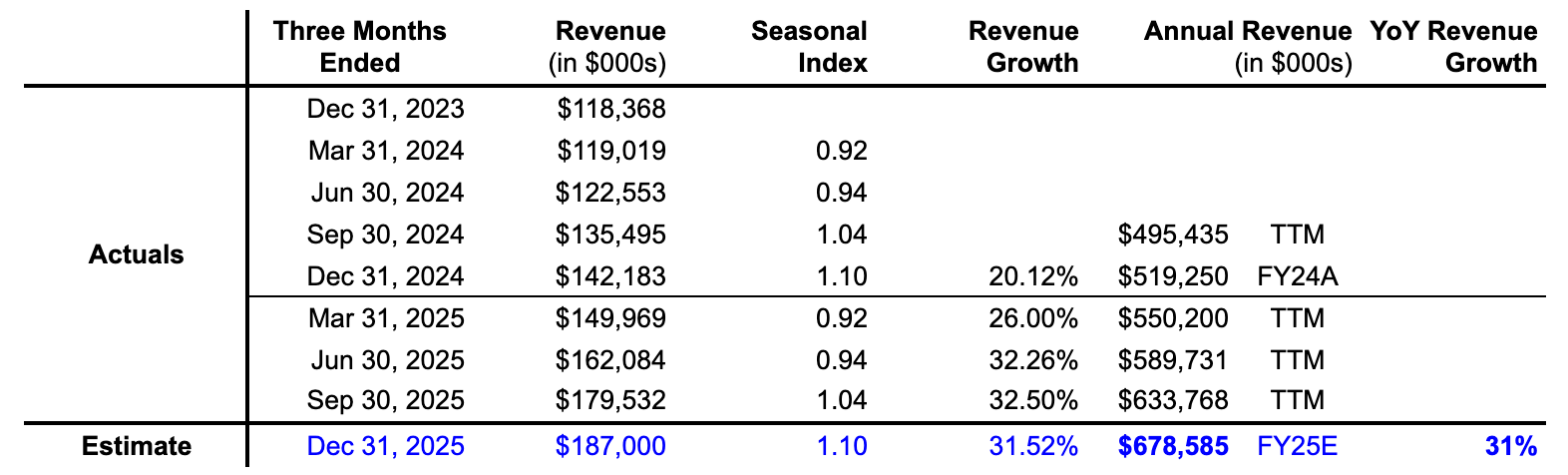

Revenue History: Liftoff’s S1 filing provided data for FY23 and FY24, along with data for the 9 months ending in September 2024 and 2025. The filing also provided eight quarters of revenue data from 4Q23 to 3Q25 (see table below).

We decomposed the 2024 quarterly data into a seasonal index and took a whack at estimating what Liftoff will report for Q425 and FY25 in its next filing. If the seasonal index is consistent from 2024 to 2025, we get $187 million in 4Q25 revenue and $678 million for the FY25. If our revenue estimate is accurate, then YoY revenue growth for Liftoff is quite healthy at 31%.

As pointed out by Brian Wieser at Madison & Wall:

“Liftoff is a smaller peer when compared with AppLovin. But it is pursuing the same strategy: building a single platform that controls both ad buying and app monetization and using its data to improve performance over time.”

On a trailing 12-month basis from 3Q25 reporting, AppLovin’s revenue is $6.3 billion, or over 9x larger than Liftoff. According to ChatGPT and app tracking service 42matters, Apple’s App Store and Google Play publish ~1,700 new apps every day. We assume a decent portion seek the kinds of services provided by companies like AppLovin and Liftoff.

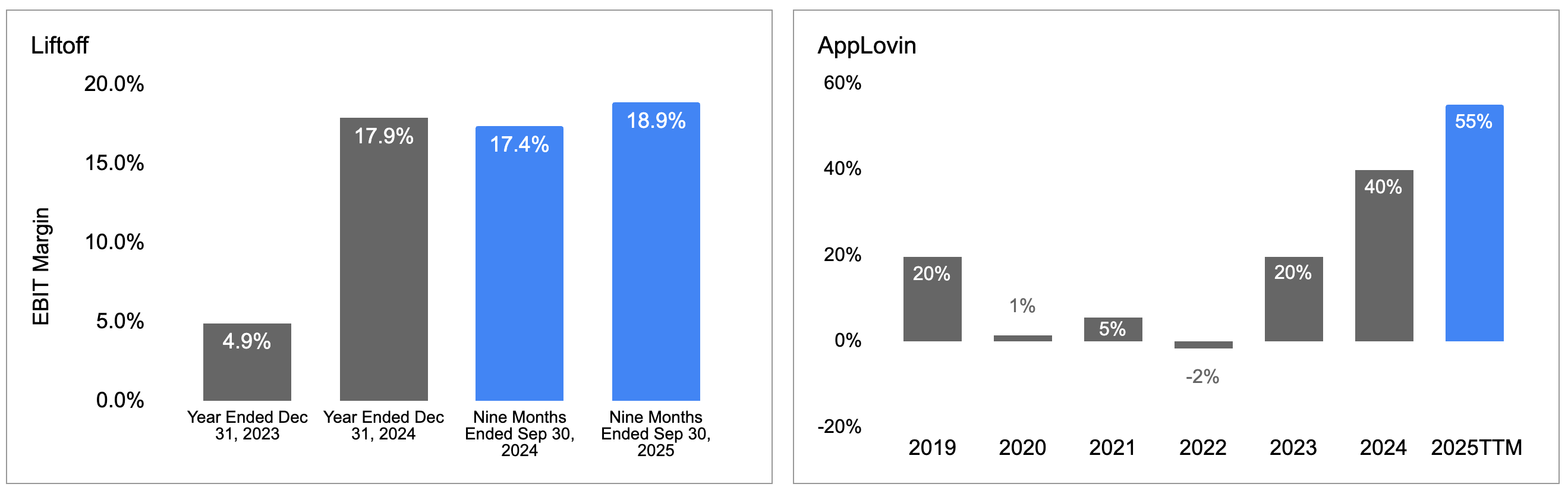

Operating Profit: Turning to operating profit margins (EBIT), Liftoff generated a material jump from 4.9% in FY23 to 18% in FY24, and has sustained that level through 2025. As we’ve pointed out in previous posts, achieving EBIT margins greater than 20% across all NASDAQ-listed companies is a low-probability event.

Notably, AppLovin is in a different class with 40% EBIT margins in 2024 and trending higher (~55%) on a TTM basis as of 3Q25 reporting.

Flywheel Business Model

Those are insane operating margins. So, before moving on, let’s take a step back to examine the basics of AppLovin/Liftoff’s flywheel business model:

App developers want revenue, so they plug tools into their apps (ad mediation + in-app bidding) to maximize ad yield across many ad buyers.

App advertisers want efficient user acquisition (UA), so they buy ads through AppLovin/Liftoff’s demand-side products to acquire users at the lowest cost possible.

More spend + more inventory = more data. As more ads run across more apps, AppLovin/Liftoff gains more signal about what works, e.g., which creatives, audiences, placements, and times drive installs and downstream value.

Better targeting/optimization improves results. Their optimization engines use that data to improve performance, e.g., lower CPI, better ROAS for app advertisers.

Better performance attracts more advertisers and spending. If app advertisers hit their ROI goals more consistently, they write a blank check.

More advertiser demand increases publisher revenue as more demand increases competition for impressions, which generally increases eCPMs and monetization for developers.

Higher publisher revenue attracts more apps. More developers integrate, adding more inventory, and the loop repeats.

Net Operating Profit After Cash Taxes (NOPAT)

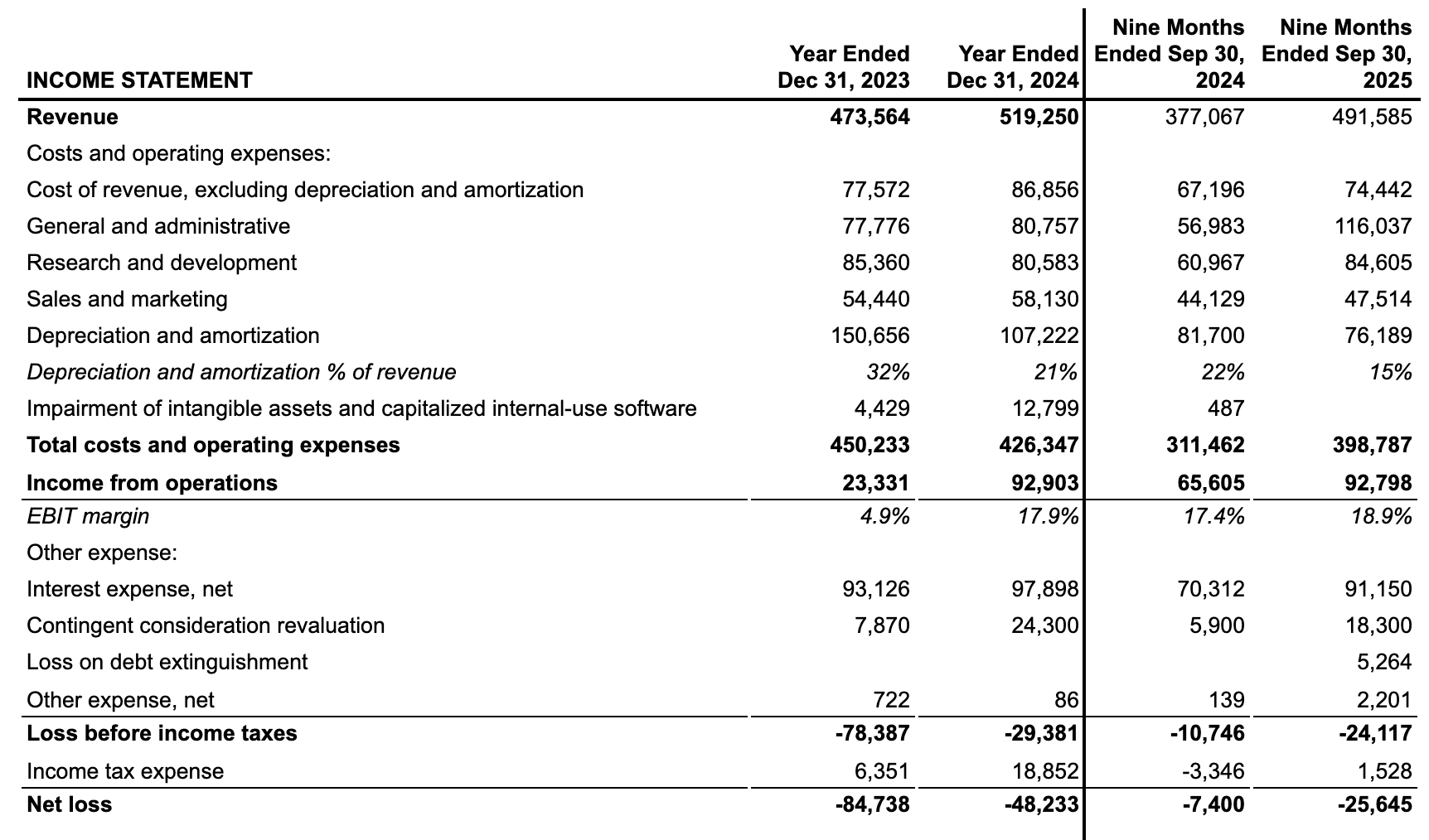

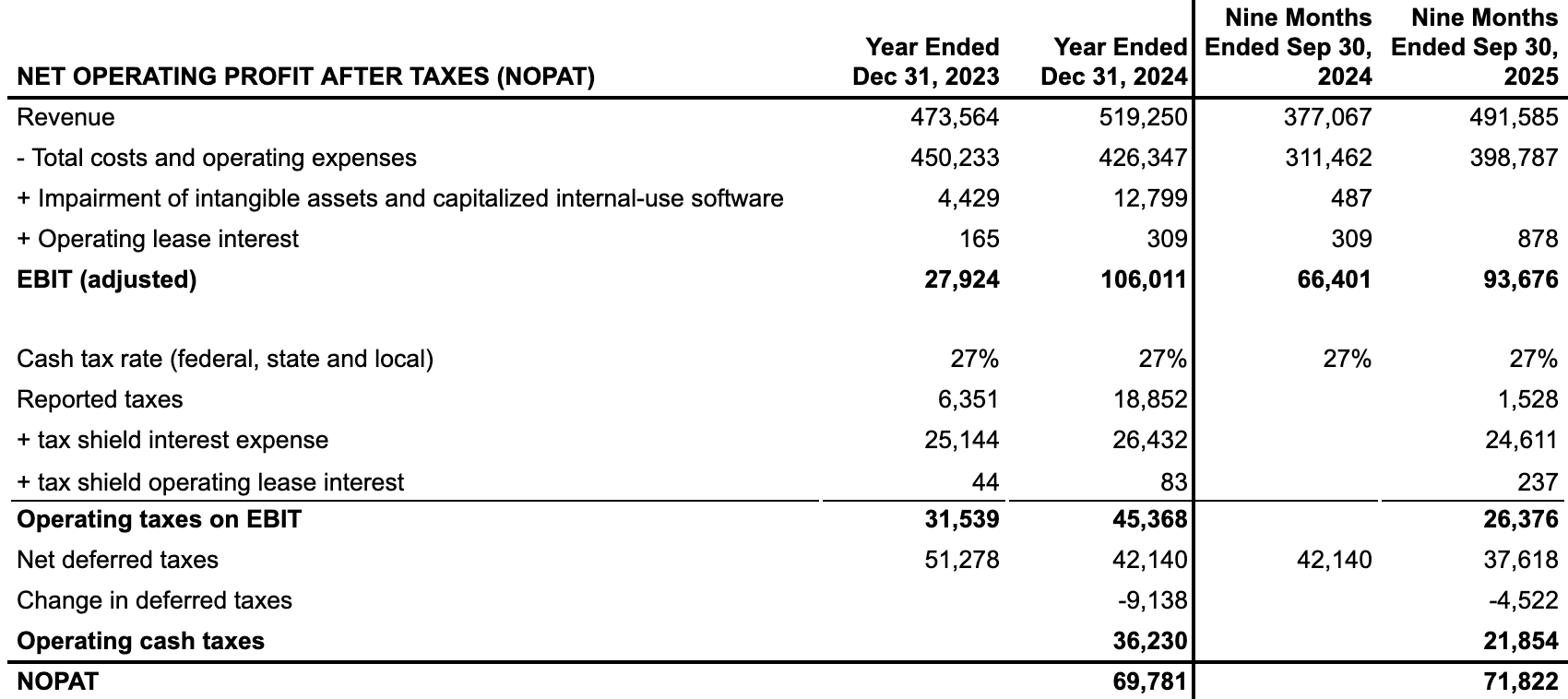

Looking at Liftoff’s income statement, we make a few adjustments to get a pure view of operating vs. non-operating performance. The first adjustment we make is the difference between reported taxes and cash taxes on an all-equity basis.

Although minor, we first add operating lease interest expense based on the reported operating lease liability sitting on the balance sheet. We apply a BBB interest rate (AppLovin is rated BBB according to S&P Global). We also add back impairment expense (a non-operating expense) to get the purest sense of operating profit possible (Adjusted EBIT).

As mentioned above, Liftoff has $1.8 billion of long-term debt, resulting in $98 million in FY24 interest expense and $91 million through 3Q25. Since these are flows to debt holders, we add back the tax shield effects of interest expense based on a 27% marginal cash tax rate (federal, state, and local tax rate assumption).

The last adjustment to make before arriving at our cash tax estimate is to account for the YoY change in deferred tax liabilities.

We estimate actual cash taxes of $36M in FY24 and $21M for the first 9 months of 2025. Unsurprisingly, the difference in cash taxes (what you cannot avoid paying at some point) and reported taxes on the income statement (GAAP accounting, timing differences) is material to equity holders.

After accounting for cash taxes, Liftoff generated $70M in FY24 in pure operating profit (13.4% margins) and $72M through the first 9 months of 2025.

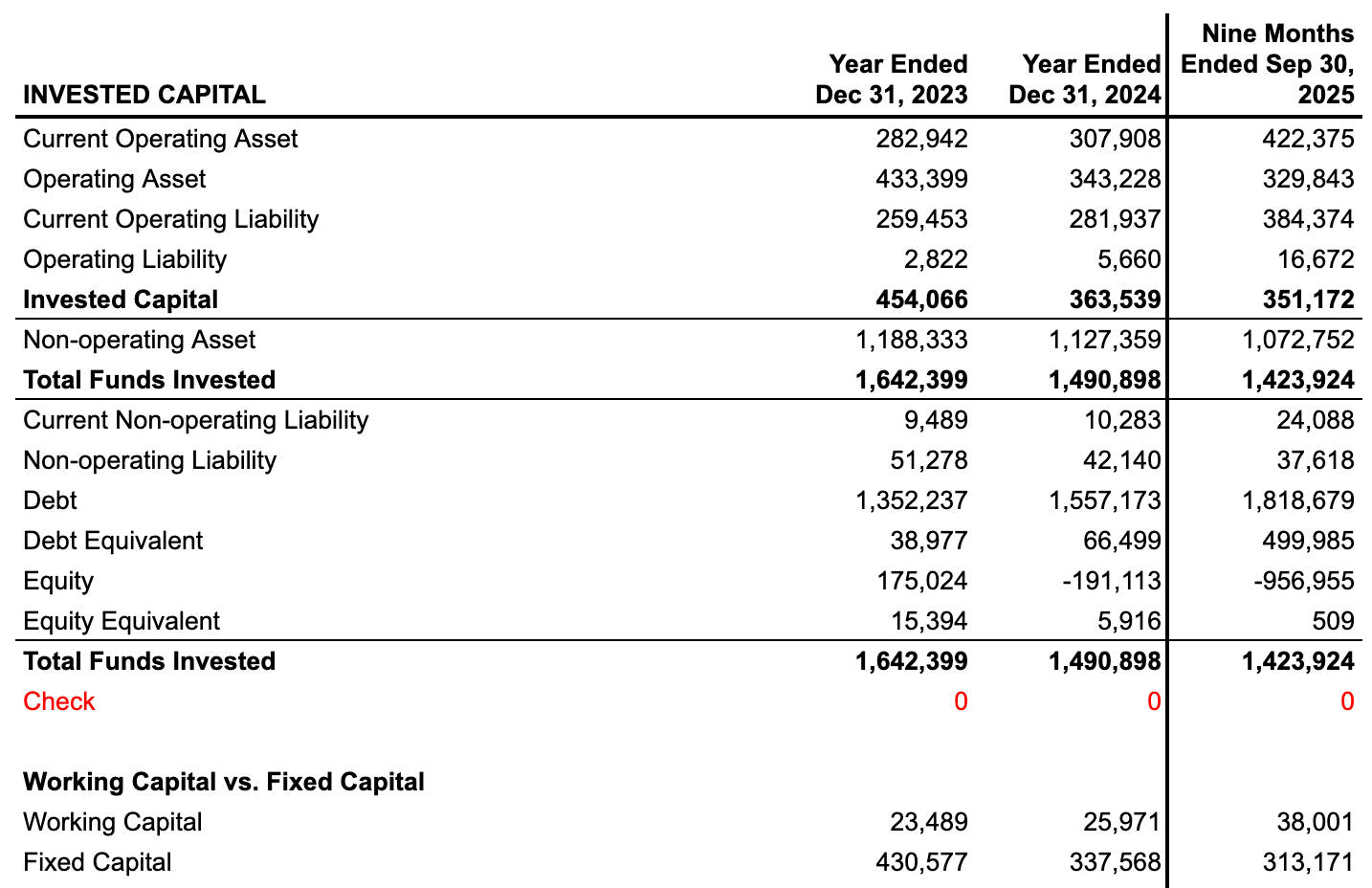

Invested Capital

Now we turn to a few balance sheet adjustments to identify operating assets and liabilities vs non-operating items to get a decent view into invested capital. The first adjustment is in “Other Assets,” where we reclassify interest rate swaps as non-operating and keep the remaining portion as operating assets.

The second adjustment is on the liabilities side, where we reclassify “Contingent Consideration” (earn-out payments to former stockholders of Liftoff Mobile) as non-operating and keep the remaining portion as operating liabilities.

The last material adjustment we make is to remove goodwill from invested capital as a non-operating asset. FWIW, we strip goodwill out of invested capital because it’s a purchase-accounting plug that reflects what the acquirer paid, not incremental operating assets deployed.

Retained Earnings/Losses

The first thing our eyes go to on Liftoff’s balance is –$1 billion in retained losses. Interestingly, AppLovin went public in April 2021 and also had –$1 billion in retained losses in FY21. However, post-IPO AppLovin’s fortunes changed dramatically with retained earnings standing at +$1B as of 3Q25 reporting. That’s a $2 billion swing.

Invested Capital

Liftoff produced respectable Return on Invested Capital (ROIC) in FY24 at 19.2%. We estimate FY25 will be around 24% and rise over the coming years. FWIW, AppLovin’s ROIC in FY24 was a whopping 73% and might go higher in FY25.

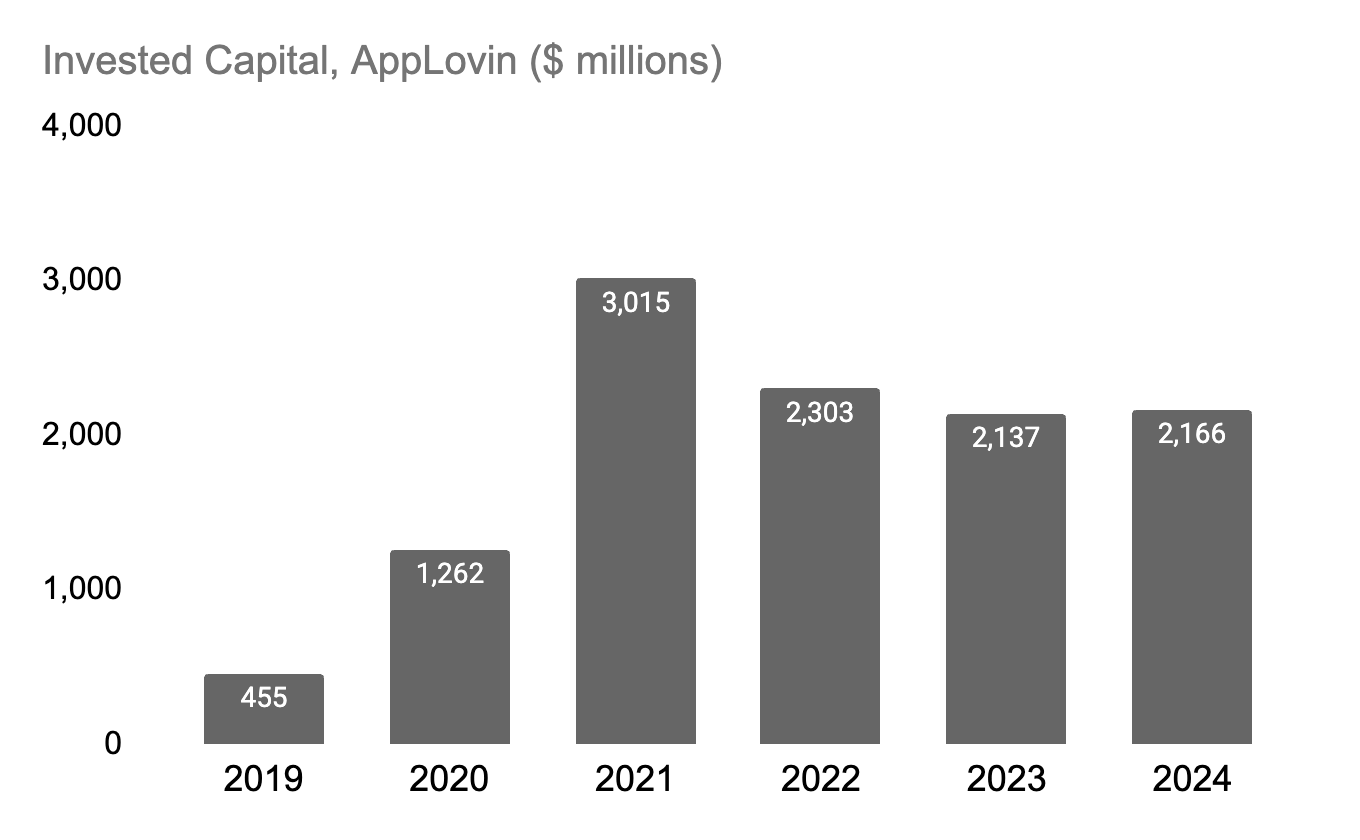

One thing to keep an eye on with Liftoff is the downward trend in invested capital. Between FY23 and FY24, invested capital decreased by 20% and by another 3% as of September 2025. This non-investment trend seems to be sector-specific because AppLovin is also not investing back into its business. We find that a bit odd because with such a high ROIC and a large spread of its cost of capital (large economic moat), you’d think a company would be investing as much as possible to grow and protect it.

When companies don’t invest in new invested capital, investors should be wary of future growth prospects. For instance, if you look at Google and Meta, you’ll find that both companies invest 20%+ per year in new invested capital during normal years. With the AI arms race in play over the past year, investment in new invested capital for Google and Meta is 30%+.

In any case, we think rational investors should take note and expect the same bold thinking from any advertising platform that is serious about winning, building an economic moat, AND sustaining it well into the future.

Valuation

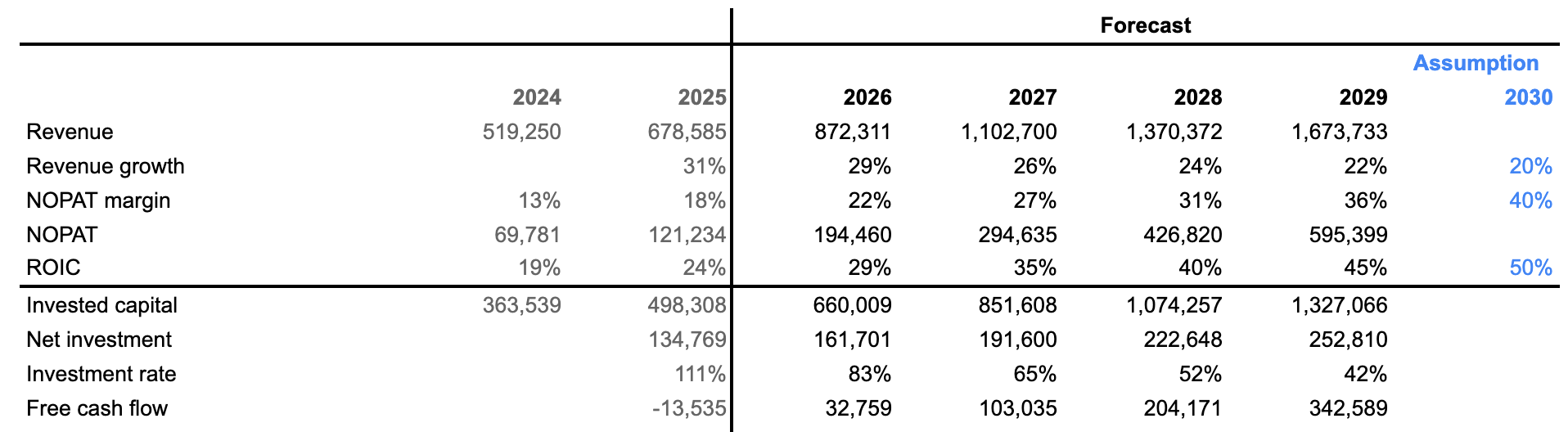

When it comes to valuation in general, we prefer taking an optimistic approach (heroic assumptions) with forecast assumptions to arrive at what the highest valuation could be and get a directional idea of where Liftoff’s IPO valuation might land.

Let’s start with revenue growth at 31% in FY25, and gradually move downward to a 20% target value in 2030. If that happens, Liftoff’s average annual revenue growth would be 25%. We think that would be phenominal growth. That said, with the potential for so many new-AI apps coming online, our growth 25% rate could also be on the light side. Time will tell.

AppLovin’s NOPAT margins were 33% in FY24, Liftoff’s were 13%. We estimate that AppLovin’s margins will surpass 40% when they report FY25. That’s an insanely productive business model and an incredibly rare operating margin. With that in mind, we set Liftoff’s NOPAT margins to gradually grow to 40% by 2030.

Liftoff’s current ROIC sits somewhere around 24%. Applovin’s ROIC is much higher at 73% (note that Google and Meta’s ROIC are ~45% and ~40%, respectively). Let’s keep our forecast picture positive and assume Liftoff’s ROIC will reach 50% by 2030.

With just these few value drivers in mind, we derive a 5-year forecast of invested capital, net investment, and end up with a sense for operating free cash flow creation.

Capital Structure and Cost of Capital

AppLovin’s capital structure is 95% equity and 5% debt. What’s more interesting is how it trades at a very high 2.5 beta, resulting in a high cost of equity of around 14%.

We noted above that Blackstone reported valued Liftoffat $4B. If we assume their valuation is enterprise value with $1.8 billion in debt, then the equity portion in 2025 would be 55% and the debt at 45%.

As noted above, post-IPO funds will be used to pay down the debt, so we assume 2026 equity/debt portions will be more like 90/10 and tend toward a normalized equity portion over time. We also assume the beta for the sector will move down to 1.3 over time, which is highly favorable to our equity valuation for Liftoff.

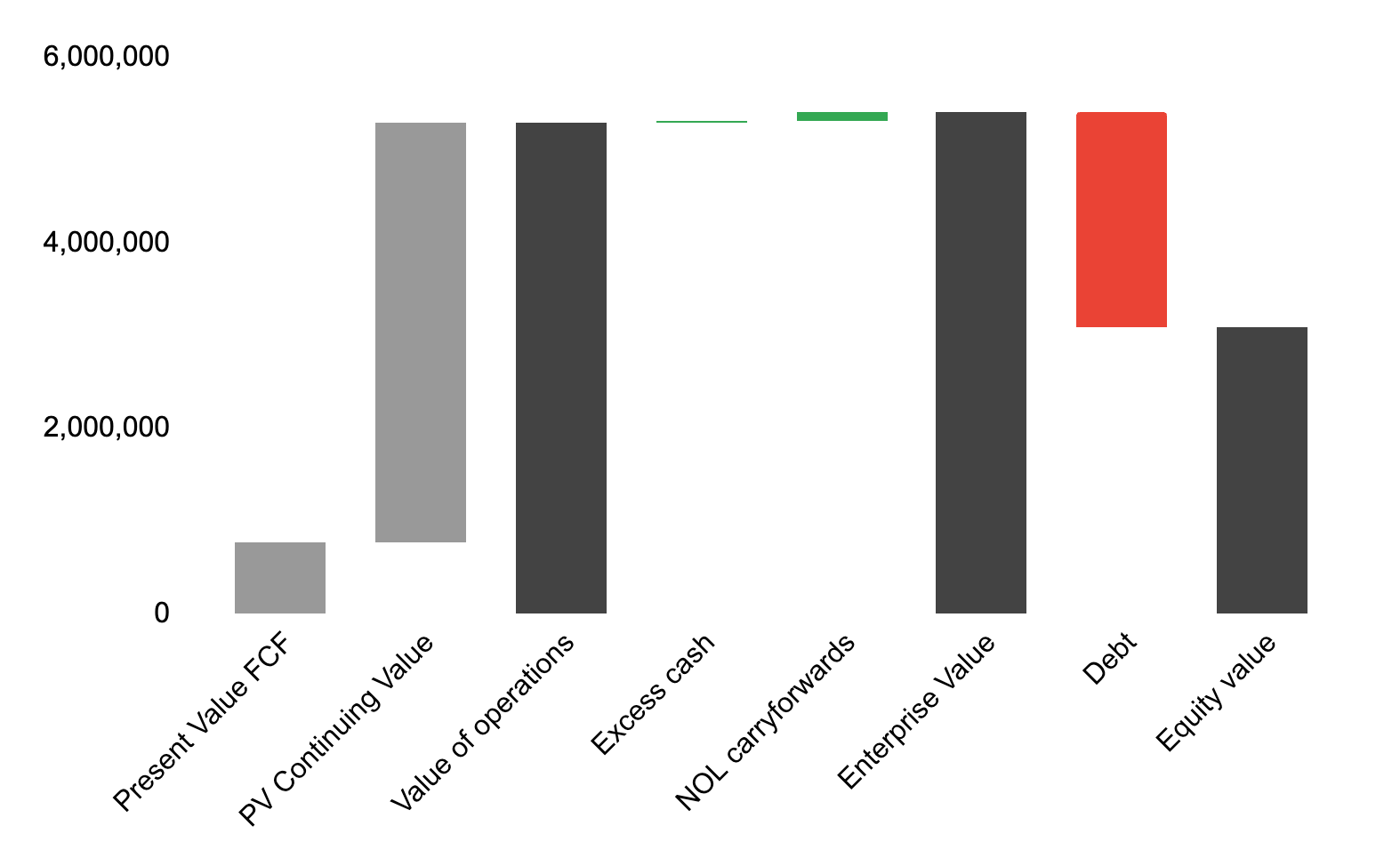

Valuation Stack: Given everything presented so far, we end with the following valuation stack for Liftoff.

$5.3 billion in operating value

Plus $14 million in excess cash today and $93 million in net operating loss (NOL) carryforwards gets us to an enterprise value of $5.4 billion.

Less current debt and debt equivalents, resulting in $3.1 billion in equity value or $29/share based on 106 million common shares.

As we mentioned above, “We have a feeling the IPO will likely trade higher than our estimate”. Here’s why…

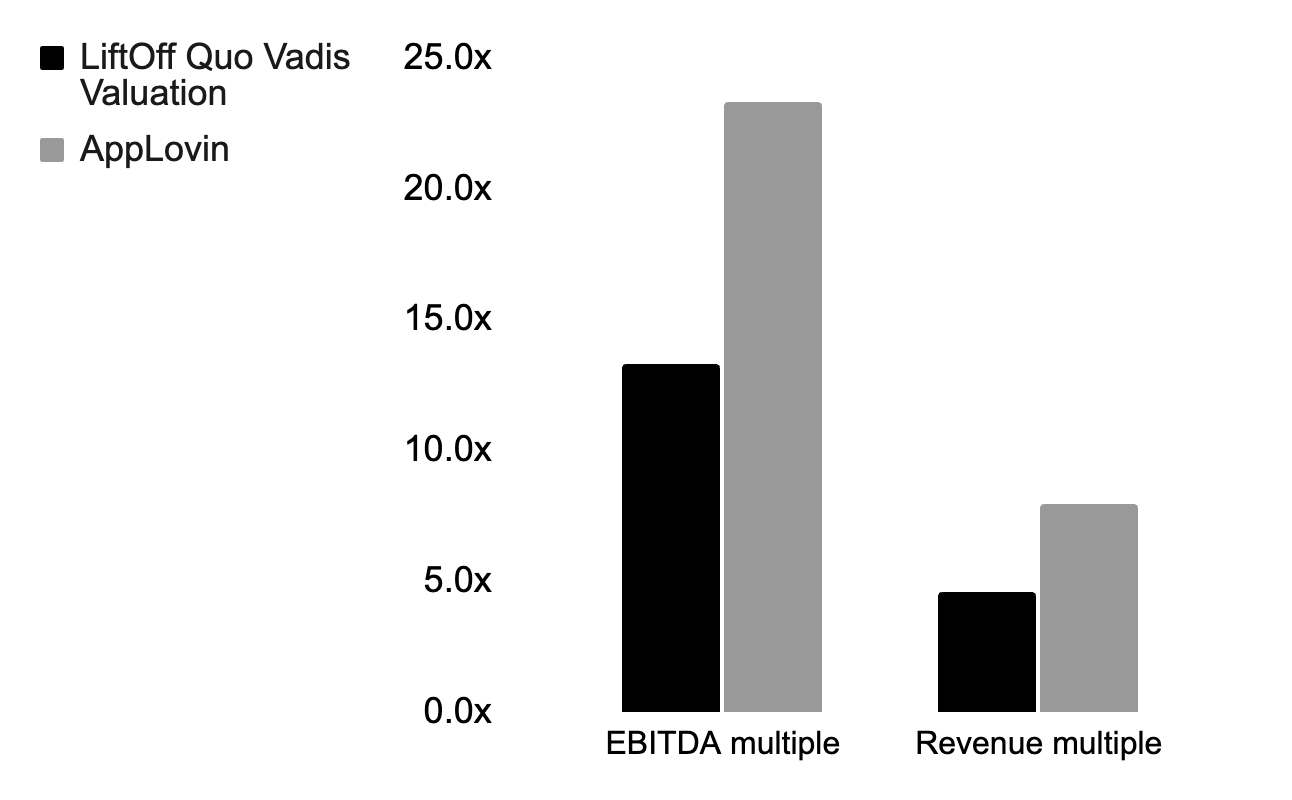

If investors simply apply AppLovin’s EBITDA or revenue multiple to Liftoff’s FY25 revenue, you could see an IPO equity value around $5.4 billion.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.

Good point. Over the long run, companies can never escape the reality of how reinvestment rates track with sustained revenue growth rates. The interesting thing about decomposing financials into operating vs nonoperating is seeing how a negative investment rate is additive to free cash flow. In other words, companies are not generating FCF from P&L but from reductions in the balance sheet. No bueno!

Brilliant breakdown of the cash tax vs reported tax implications here. The observation about declining invested captial despite 24% ROIC is something I've noticed in SaaS too, where the best moats sometimes come from data network effects rather than physical assets. When platforms hit that flywheel moment, maybe reinvestment becomes more about selective optimzation than broad expansion.