#119: MNTN IPO + Valuation Update

Quo Vadis has organized pre-Cannes Webinars with two AI tech companies. One on the publisher side (June 3/10 AM ET), the other in the AI data semantics space (June 4/10 AM ET).

June 3, 10:00 ET: How AI and Dynamic Pricing Are Redefining Publisher Power with Andrew Mole (CEO/co-founder of pubX) and special guest Addy Atienza (Managing Director of Global Programmatic at The Time Out Group). Learn about the virtues of true dynamic floor pricing.

June 4, 10:00 AM ET: Data People Wanted, The Story-Driven Superpower at the Heart of Modern Decision-Making with Luke McGuinness (CEO/co-founder of Above Data) and special guest, Justin Evans, author of The Little Book of Data, aka the "Freakonomics of Data." Part Freakonomics, part career manifesto, The Little Book of Data makes the case that everyone, especially advertisers and publishers, must become fluent in data to thrive in a world increasingly run by AI and analytics.

MNTN IPO + Valuation Update

MNTN went public last week, opening at $21/share with an initial price set at $16/share, reaching a $1.5 billion valuation at the closing bell on day one and closing down at $1.3 billion on day 2 (Friday).

MNTN’s mission is to dominate the CTV market across millions of SMB advertisers. That’s undoubtedly a greenfield opportunity given Google’s, Meta’s, Amazon’s, and Criteo’s success with SMB advertisers who can finally play ball in the TV space.

As MNTN’s CEO said in the company’s February 2025 S1 filing:

“For too long, upfront financial commitments, limited access to data, and the high costs of creative production have kept smaller brands out of television advertising. We built MNTN’s self-serve platform to solve these problems and ensure that every brand, no matter its size, has the opportunity to thrive on TV. What Netflix did to television, MNTN is doing to TV advertising.” — Mark Douglas

The company is going after what it estimates to be a $60 billion to $120 billion serviceable market:

“We calculate our market opportunity using business count data sourced from Statista, focusing on the number of SMBs with 10-500 employees in 2023. Using data sourced from Zippia, businesses of this size generate, on average, annual sales of $8 million. For these businesses, data from Gartner assumes approximately 10% of sales go to marketing, with 5% of marketing budgets allocated to PTV advertising, according to management estimates. Multiplying the number of businesses with 10-500 employees of 1.5 million by the average PTV advertising budget of approximately $40,000 to $80,000 arrives at our SAM figure of $60 to $120 billion.” — MNTN S1 Filing

From Quo Vadis’ margin safety perspective, we think the addressable SMB/CTV market is more likely half the size at $45 billion at the midpoint because everyone who sizes CTV seems to forget that YouTube is ~50% of the market while Amazon takes up a meaningful chunk of what’s left over. It’s still a big market, nonetheless, but size still matters if we are being precise.

Sizing investor expectations of MNTN

Instead of valuing MNTN based on margin of safety assumptions like we did in our March 4 post, when the company filed its S1, what we cover attempts to answer the question:

What are investors expecting in terms of future performance expecations in order to achieve the current $1.3 billion post-IPO valuation?

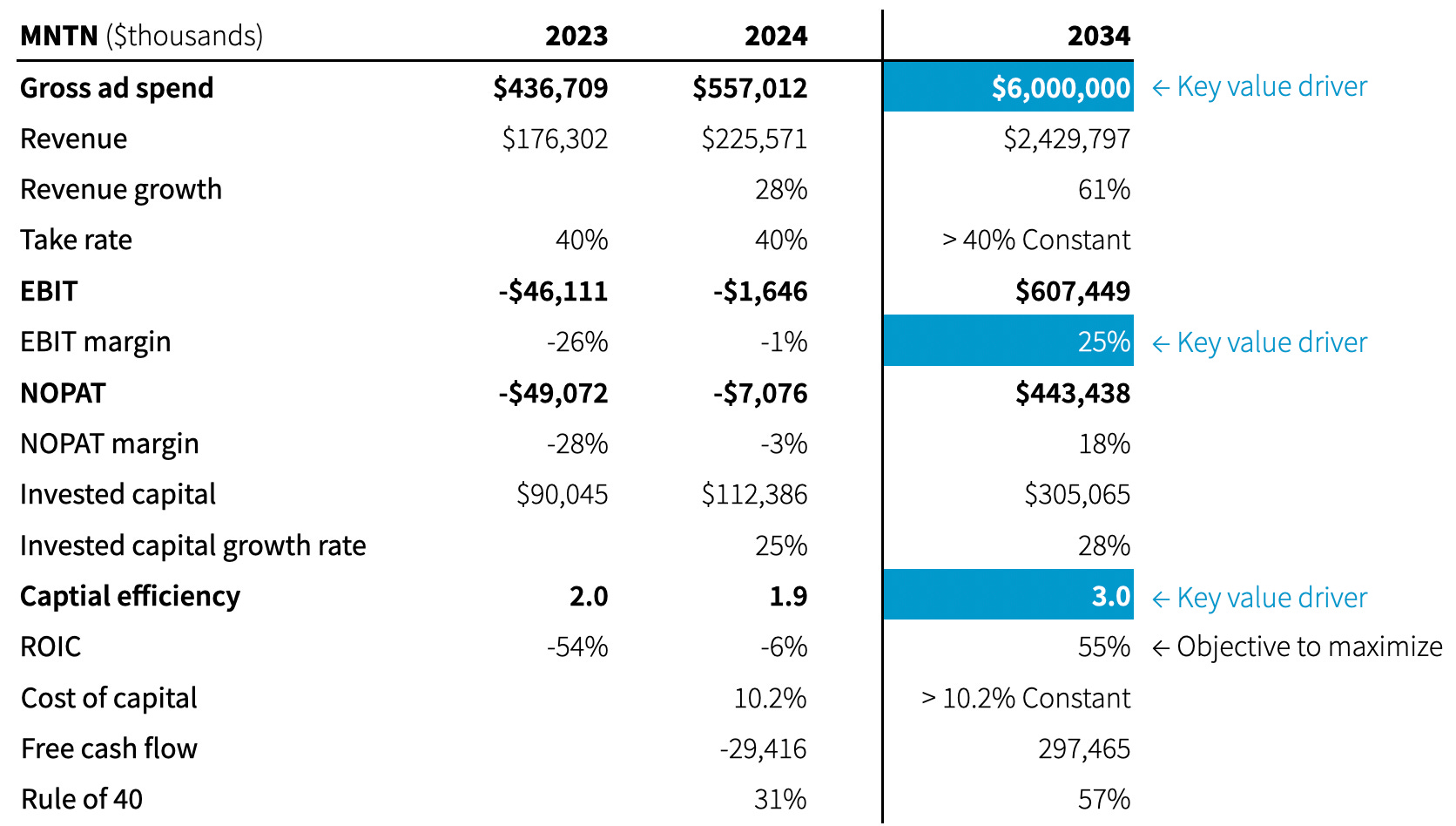

Let’s start with gross ad spend, revenue, and take rates.

Gross ad spend: The company does not disclose gross ad spend running through its platform, but it does disclose trade payables to SSPs/publishers. To fill in the blank, we assume 70 days payable and back into an implied gross spend of $557 million in FY24.

Revenue: MNTM reported $225 million in revenue in FY24 and 28% growth over FY23. That implies a 40% take rate. The average take rate for TTD, CRTO, DSP, TBLA, and OB is 35%. So, 40% take rates feel okay, even if a bit favorable to the upside for MNTM valuation.

Next, we turn to the name of the game: profitability

EBIT: Operating profits came close to reaching positive territory in FY24. Given the $1.3 billion valuation today, investors are probably expecting to see around 2% EBIT margins in FY26 with a 25% target ten years down the road in 2024. Importantly, anytime a company reaches 20%+ EBIT margins, they are performing in the top quartile.

NOPAT: Accountants live by certain rules like GAAP and IFRS, which distort the difference between the reported taxes and actual cash taxes on an as-if basis. After making tax shield adjustments for interest expenses and embedded capitalized lease interest (flows to debt holders, not equity holders) using a 27% marginal tax rate (federal, state, local), and adjusting for deferred taxes, we estimate –$7 million in NOPAT losses in FY24.

Turning to the balance sheet and invested capital. We dissected and classified each balance sheet item into operating vs. non-operating assets and liabilities, and also classified equity, debt, and equivalents like convertible preferred stock (debt).

With NOPAT and Invested Capital on our side, we arrive at the most important driver of value creation, Return On Invested Capital (ROIC), which was –6% in FY24 but greatly improved over FY24 at –54%. That means MNTN is destroying value by not achieving greater than its cost of capital, estimated at 10.2%. While negative ROIC is normal for maturing companies, it seems a bit odd for a 16-year-old company. With over half a billion in gross ad spend passing through its platform, one should expect to see better performance at this point, particularly for a public company.

Cost of Capital: Given $228 million in debt and debt equivalents, and a market cap of $1.3 billion, and assuming a cost of debt of ~6% (slightly higher than AA rating) with an average public adtech beta of 1.3, we estimate cost of capital at 10.2%

Free cash flow: Net invested between FY23 and FY24 was $22 million (the YoY change in investments in working capital and capex). Given –$7 million in NOPAT, MNTN burned –$29 million in free cash flow in FY24. Again, we’d expect better performance for a company as old as Criteo and nearly as old as The Trade Desk (more on that comparison below).

Looking ahead to investor expectations in 2034

The trickiest thing about forecasting is deciding how long the forecast should be. We usually use a five-year forecast for public companies with a long enough historical track record. In MNTN’s case, we taking it out ten years to satisfy our need for margin of safety.

The big question is: What will revenue be in 2034? From a valuation perspective, the four biggest drivers in our discounted cash flow model are:

NOPAT margins in the future, growing to a 25% target in FY34.

Take rates, we assume 40% constant in our model.

Improving capital efficiency from 2.0 to 3.0, which means we expect the amount of revenue generated from $1.00 in new invested capital to improve over time.

The ability to attract gross spend from SMB marketers looking to place ads in CTV environments.

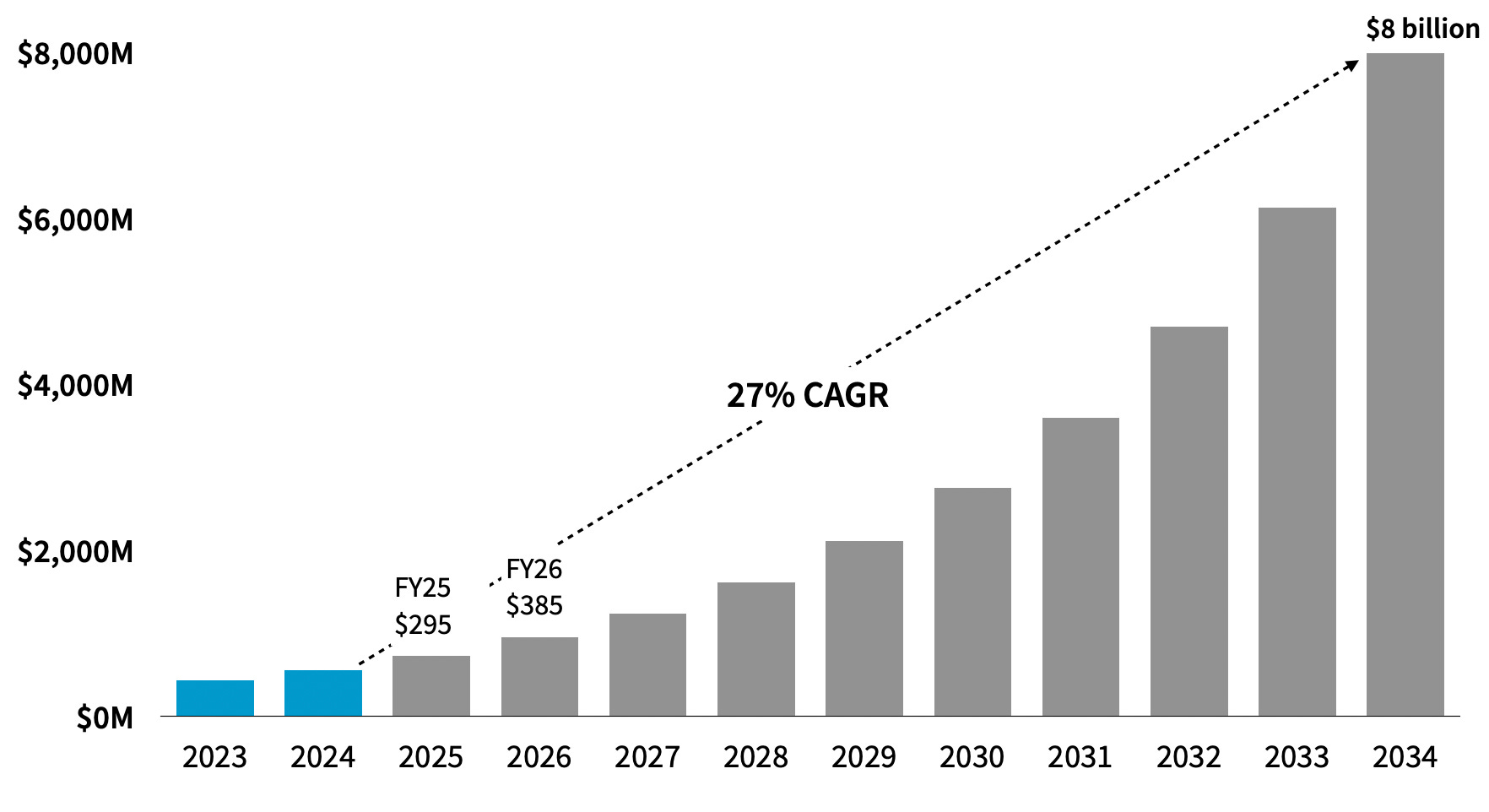

Given these key value drivers and MNTN’s current equity valuation, our discounted cash flow model indicates investors need to see $6 billion in gross ad spend by 2034. That’s a lot of selling.

If the trend line is true, MNTN will generate around $295 million and $385 million in revenue in FY25 and FY26, respectively.

MNTN Valuation Stack

Assuming investors are right that MNTN drives significant revenue growth by attracting thousands of SMB advertisers to CTV with strong ROI, with operating profit margins growing to 25%, they’re effectively betting on highly disciplined execution and a highly efficient model. At its core, this belief reflects confidence that management will make great things happen. That’s an interesting bet in a space where high financial achievement is the exception, not the rule (only Trade Desk and Criteo have truly passed the test over the years since their IPOs).

What do the comps say about revenue expectations?

Here’s the challenge we see for MNTN. The company is 16 years old, but only generates $225 million in revenue. If the history of comparable companies in the adtech space offers any indication of the present and future, they would tell us that MNTN is way behind.

At Sweet 16, The Trade Desk had $1.2 billion in revenue, Criteo had nearly a billion, and Magnite had $468 million, but MNTN only had $226 million on its 16th birthday in 2024.

Looking out three years down the road when MNTN turns 19, which is Criteo’s age this year, it will still be way behind where it needs to be to meet investor expectations today.

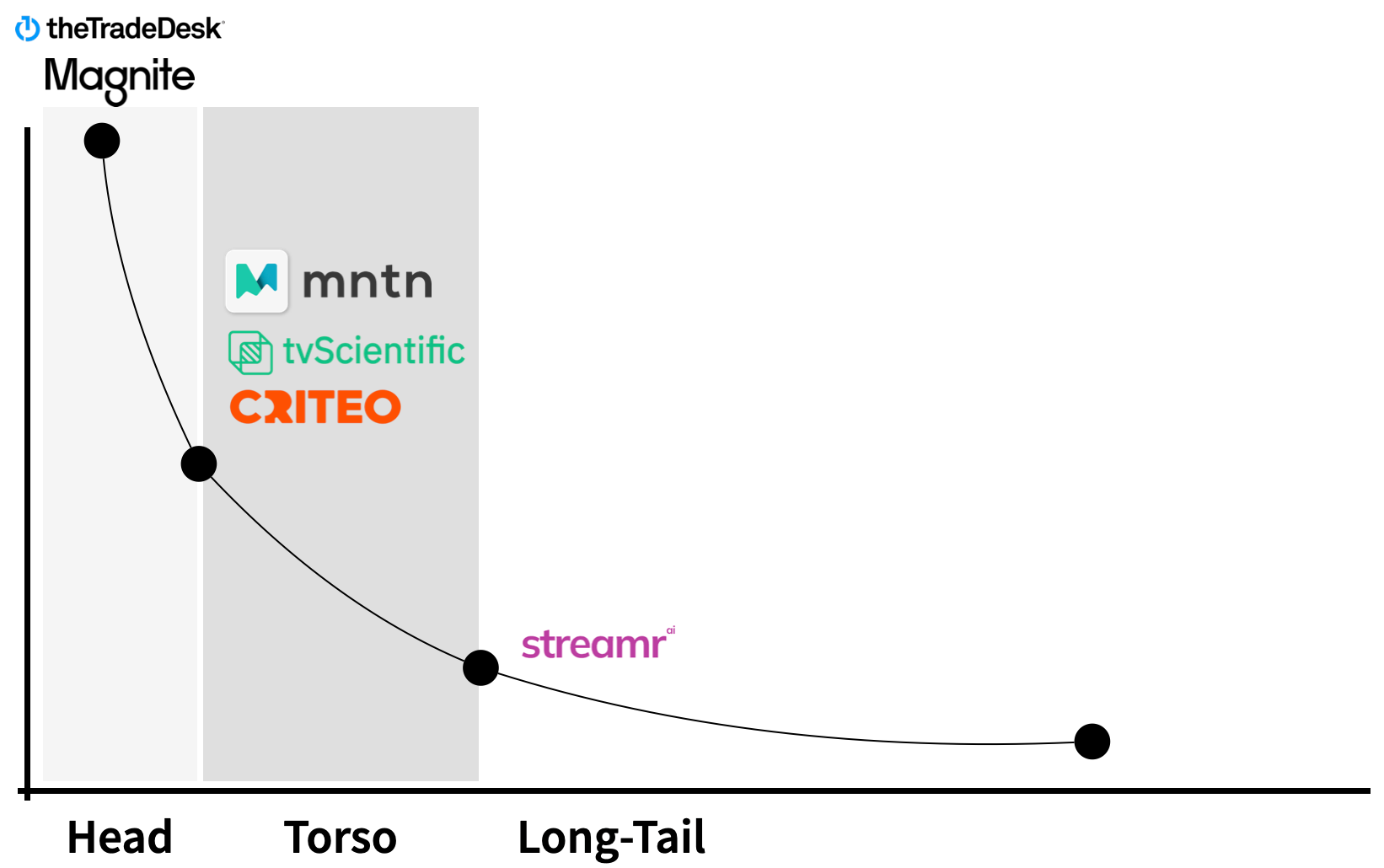

What about competition?

MNTN’s stated strategy is to play in the SMB space by offering technology and access to CTV ad inventory. It’s a big space and a big opportunity with many competitors eyeing the same prize.

For instance, The Trade Desk already has a nice position at the head of the long-tail. As TTD looks to sustain growth, it could easily unleash its sales force and management discipline into the torso of SMB advertisers.

From a supply-side perspective, Magnite (and other SSPs like PubMatic and Index Exchange) are forging direct access relationships to buyers, and they are also well-positioned to front CTV inventory.

In the torso, MNTN will find competition from the likes of well-funded companies like TVScientific and others.

Criteo is the most obvious potential competitor, even though the company has not placed any big bets on CTV as it focuses on growth by powering retail media. That said, with an army of engineers and salespeople in 30+ markets around the world, and the second biggest trove of conversion/shopper data (Amazon has the most), Criteo has a massive opportunity to play in the closed-loop space.

Looking at the long tail, companies like Streamr.ai offer plug-and-play AI for smaller SMBs to activate CTV campaigns in one step. We expect a ton of competition in this area and a few M&A quick-wins too.

AdTech IPOs vs. Good AdTech IPOs

The adtech market has been waiting a long time for a fresh IPO. But in the collective rush and lust for exits, whether by venture capital, private equity, or M&A bankers, it’s worth remembering that simply going public isn’t enough. The IPO has to work. If, in a few years, the market reprices expectations downward and the stock trades significantly below its IPO valuation, then adtech just becomes another cautionary tale instead of a success story. That’s bad for adtech.

Only good IPOs — those that deliver on expectations and create long-term value — are good for the next cycle of a healthy and clean ecosystem.

The trade record is not great. That’s why pre-mature IPOs should hold off, or else it can tarnish the adtech industry. Looking across the 16 public adtech companies that Quo Vadis tracks, only three are trading above their IPO price, and only three deliver meaningful ROIC: TTD, APP, and CRTO. We hope MNTN becomes one of them.

Disclaimer: This post, and any other post from Quo Vadis, should not be considered investment advice. This content is for informational purposes only. You should not construe this information, or any other material from Quo Vadis, as investment, financial, or any other form of advice.